As the curtains close on FY26, the provisional data floodgates have opened. From the “Retail-first” pivot in Indian banking to a historic anomaly in global oil markets, here is everything you need to know about the current state of the markets.

🏛️ THE BANKING SECTOR: The Battle for Deposits

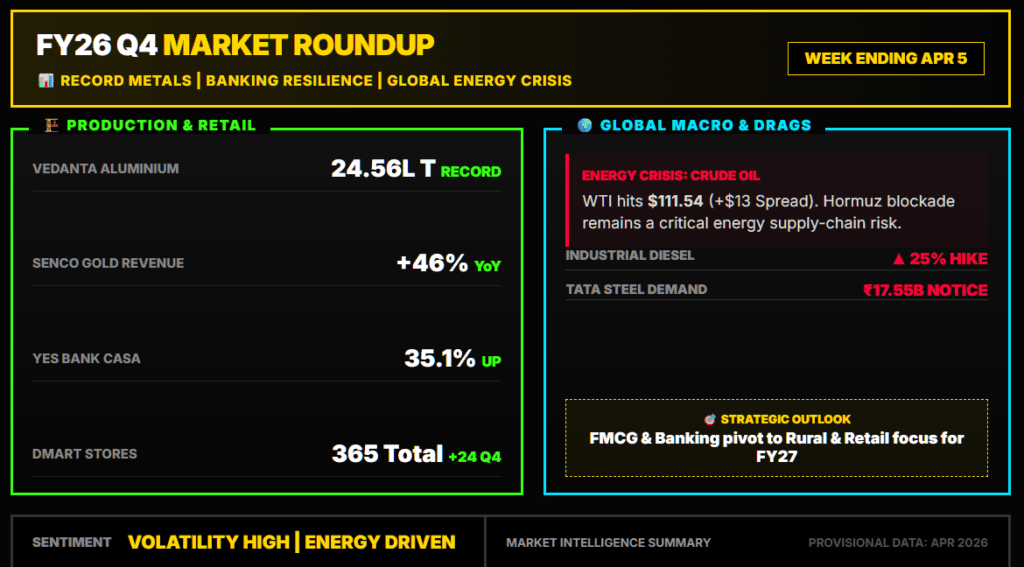

The Q4 provisional updates reveal a sector fighting hard for liquidity while maintaining robust credit growth.

- HDFC & Kotak Lead: Kotak Mahindra Bank reported a steady 16% YoY growth in advances, while rumors swirl about its potential acquisition of Deutsche Bank’s India retail business.

- The CASA Comeback: Yes Bank saw its CASA ratio improve to 35.1%, with deposits crossing the ₹3.18 Lakh Cr mark. IDFC First Bank also hit a record CASA ratio of 49.8%.

- Retail Pivot: Bandhan Bank is aggressively shifting away from bulk deposits (-6.9%) to retail term deposits (+30%), while ESAF SFB saw a massive 38% surge in its retail loan book.

- Milestones: IDBI Bank officially crossed the ₹6 Lakh Crore total business milestone, even as the stock faces a 33% YTD correction.

🏭 METALS & INFRA: Shattering Production Records

Operational efficiency was the theme for India’s heavyweights this quarter.

- Vedanta’s Record Year: Despite a 16% dip in Oil & Gas, Vedanta hit “highest-ever” annual production in Aluminium (24.56L Tonnes) and Alumina. Its Zinc business also touched new peaks.

- Order Wins: J Kumar Infra bagged a mega ₹1,184 Crore EPC contract for the Lucknow International Convention Centre.

- Regulatory Hurdles: Tata Steel is bracing for a legal battle after receiving a ₹17.55 Billion demand notice over alleged excess coal mining—a claim the management calls “unjustified.”

🛒 CONSUMER & FMCG: Wedding Bells & Rural Recovery

The consumer story in Q4 was a tale of two halves: domestic resilience vs. international headwinds.

- Senco Gold’s Surge: Revenue jumped a staggering 46% YoY, proving that even doubling gold prices couldn’t stop the Indian wedding season demand.

- Adani Wilmar (AWL): Edible oil volumes grew 17%, with Quick Commerce emerging as a powerhouse channel (+46% growth).

- Dabur’s Dilemma: Domestic FMCG is recovering well (High-single digits), but geopolitical tensions in West Asia are dragging down international business.

- Leadership Shifts: Devyani International overhauled its C-suite for Pizza Hut and Costa Coffee, signaling a major strategic reboot for FY27.

🌍 GLOBAL MACRO: The $110 Oil “Nightmare”

Geopolitics has officially taken the wheel of the global energy market.

- WTI Historic Anomaly: For the first time since 1983, the WTI front-month spread hit a $13.50 premium, as traders scramble for immediate physical supply amid the Iran war.

- Hormuz Blockade: While 7 Indian LPG tankers (including Green Sanvi) have successfully navigated the Strait of Hormuz, the route remains under tight Iranian watch.

- Domestic Fuel: While retail petrol/diesel remains steady, Industrial Diesel prices were hiked by 25% to ₹137.81/L, and Commercial LPG spiked by ₹195

The markets are currently rewarding volume growth and operational efficiency (Vedanta, Senco, DMart) but remain wary of regulatory risks (Tata Steel) and global supply chain shocks (AWL, Fuel).

As we head into the full earnings season, the focus remains on whether FY27 can maintain this momentum amidst a volatile global backdrop.

What is your top pick for FY27?

🏦 Banking | 🏗️ Infra | 💍 Consumer | 🛢️ Energy