The Capital Asset Pricing Model (CAPM) is a formula used to estimate the expected return of an investment based on its risk compared to the overall market. It helps investors understand the trade-off between risk and return.

Table of Contents

What Is CAPM?

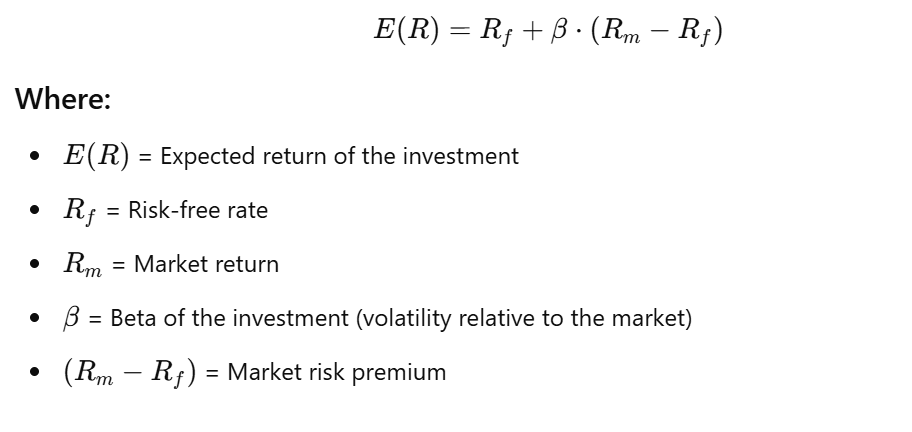

The basis of the CAPM is the correlation between the beta of an asset, the risk-free rate (usually the rate on Treasury bills), and the equity risk premium, which is the market’s expected return less the risk-free rate.

CAPM Formula and Calculation

Example of CAPM

- Risk-Free Rate (rf) = 3.0%

- Beta (β) = 0.8

- Expected Market Return (rm) = 10.0%

- Equity Risk Premium (ERP) = 10.0% – 3.0% = 7.0%

Investors expect to be compensated for risk and time value of money. The risk-free rate in the CAPM formula represents the time value of money. The remaining components of the CAPM formula account for the investor’s additional risk.

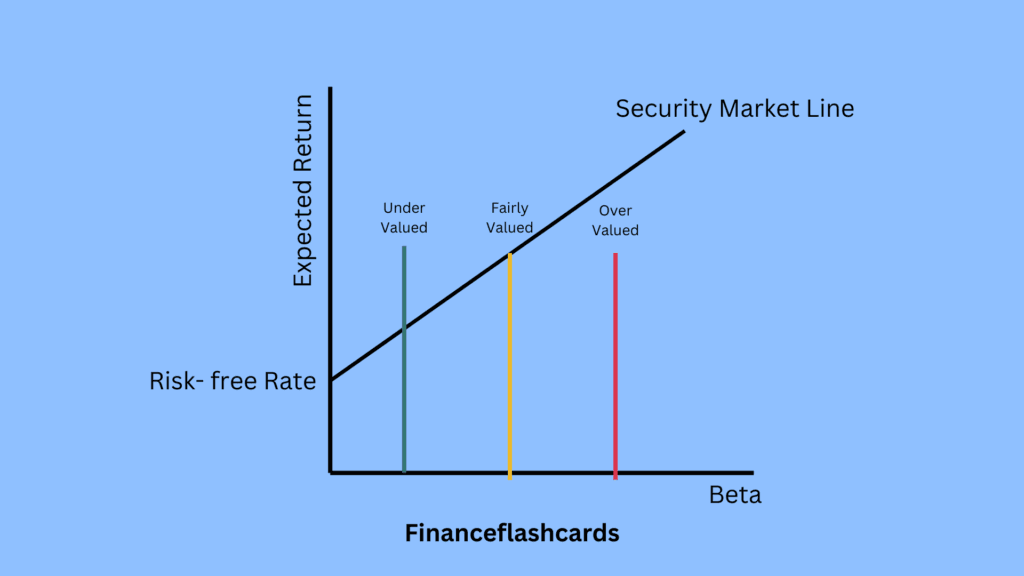

CAPM also helps determine if an investment is undervalued or overvalued by comparing its expected return (using CAPM) with its actual return:

Undervalued: If the actual return > expected return (good investment opportunity).

Overvalued: If the actual return < expected return (less attractive).

For Example

If the risk-free rate is 4%, the market return is 10%, and the stock’s beta is 1.2, the expected return using CAPM is calculated as

E(R)=0.04+1.2⋅(0.10−0.04)=11.2%.

If the stock’s actual return is 12%, which is higher than the expected return, the stock is undervalued, making it an attractive investment. Conversely, if the actual return were lower than 11.2%, the stock would be overvalued

What are the CAPM Theory Assumptions?

The capital asset pricing model (CAPM) is based on two core assumptions from Modern Portfolio Theory (MPT)

Efficient Markets (Competitive): Financial markets are competitive and efficient in terms of information collection, which influences the pricing of securities in the markets; however, identifying market mispricings becomes increasingly difficult.

Rational investors: Financial market participants are generally assumed to be rational, risk-averse investors.

- Risk-Free Borrowing and Lending: Investors can borrow or lend unlimited amounts at the risk-free rate.

- Single Period Investment Horizon: All investors have the same time frame for their investment decisions.

- Diversified Portfolios: Investors hold diversified portfolios to eliminate unsystematic risk, focusing only on systematic risk.

- Homogeneous Expectations: All investors have the same expectations for risk, return, and correlations of assets.

- No Taxes or Transaction Costs: There are no taxes, transaction costs, or restrictions on trading.

- Risk Measured by Beta: The risk of an asset is entirely captured by its beta, reflecting its sensitivity to market movements.

As a result, it remains unclear whether CAPM works. Beta is the main sticking point. When professors Eugene Fama and Kenneth French examined share returns on the New York Stock Exchange (NYSE).

They discovered that long-term differences in betas did not explain the performance of various stocks. Over shorter time periods, the linear relationship between beta and individual stock returns breaks down as well. These findings seem to indicate that CAPM may be incorrect.

Alternative to CAPM

While CAPM is widely used, it has limitations and does not account for some market complexities. To address these issues, several alternative models have been developed that provide a more complete picture of asset pricing.

These alternatives, such as the Fama-French Three-Factor Model and Arbitrage Pricing Theory (APT), introduce new variables to better capture the various factors influencing returns.

The Fama-French Three-Factor Model expands on CAPM by adding size and value factors to better explain market anomalies.

Arbitrage Pricing Theory (APT) offers flexibility by using multiple factors like inflation and GDP growth.