Financial discipline is the cornerstone of long-term financial success, yet many Indians struggle to maintain it amid daily expenses, loans, lifestyle inflation, and changing priorities. Wouldn’t it be great if you could quantify your financial discipline into a simple score – a number that tells you how well you manage your money and where you stand on your financial journey?

This blog introduces the idea of a Financial Discipline Score – a simple, 100 – point scoring system based on ten key parameters that reflect how disciplined you truly are in managing your money. Through this, readers will be able to self-assess, understand their strengths and weaknesses, and act to progressively improve their financial health.

Table of Contents

The Financial Discipline Score Framework

Each of the ten parameters below can be scored between 0 to 10 points depending on your habits and status. Add them up for a maximum possible score of 100.

The following sections break down each parameter with scoring guidelines and real Indian examples for clarity.

Savings Ratio (0 – 10 points)

Your savings ratio is a vital measure of financial discipline – the percentage of your monthly income regularly saved or invested.

Formula: Savings Ratio = (Monthly Savings / Monthly Income) × 100

20% or more savings ratio: 10 points

15%-20%: 8 points

10%-15%: 6 points

Less than 10%: 3-5 points depending on consistency

Sporadic or no savings: 0-2 points

Example:

Rahul, a software engineer in Bengaluru earning ₹70,000/month, consistently saves ₹14,000 (20% savings ratio) by investing in SIPs and fixed deposits. He scores a full 10 here.

Contrast with Priya, a young professional in Pune who saves ₹5,000 irregularly some months – she would score around 4-5 points.

Expense Tracking & Budgeting (0 – 10 points)

Do you track your expenses daily, weekly, or monthly? Do you follow any budget (like the 50-30-20 rule or zero-based budgeting)? Are you consistent with a tool or app?

Consistent daily / weekly tracking + active budgeting: 10 points

Monthly tracking + following a budget: 7-8 points

Minimal or irregular tracking, no budget: 3-5 points

No tracking, no budget: 0-2 points

Example:

Sneha uses apps and Google Sheets to track her ₹50,000 monthly expenses daily and follows a zero-based budget. This earns her near perfect 10 points.

On the other hand, Anil casually reviews expenses when prompted but doesn’t budget regularly – scoring about 4 points.

Debt Management (0 – 10 points)

Evaluate how well you manage debts like credit cards, personal loans, and EMIs.

Pays credit card bills in full and on time + low debt-to-income ratio (<30%): 10 points

Maintains EMIs well and pays before due dates: 7-8 points

Relies on credit frequently and/or pays minimum dues: 3-5 points

High-interest debts without timely repayment: 0-2 points

Example:

Deepak ensured he cleared his ₹50,000 credit card bill on time monthly, avoiding interest and maintaining a 20% debt-to-income ratio – 10 points.

Conversely, Seema faced high-interest credit card debt often paying only minimum amounts – scoring about 2-3 points.

Emergency Fund Strength (0 – 10 points)

Emergency funds are crucial for unexpected expenses. Scores are assigned based on how many months of expenses you’ve saved:

6+ months of essential expenses: 10 points

3 to 6 months: 7 points

Less than 3 months: 3 points

None: 0 points

Example:

Ravi from Chennai saved 9 months’ worth of expenses for emergencies, giving him 10 points.

Sneha has about 2 months’ worth – scoring 3 points.

Investing Habit Consistency (0 – 10 points)

Look at your investing habits – do you have consistent SIPs? Diversified portfolio? Long-term mindset? Avoid stopping investments due to market fluctuations?

Consistent SIPs across equity, debt, gold + long-term mindset: 10 points

Regular SIPs but limited diversification: 7-8 points

Irregular investing, market timing attempts: 3-5 points

No investing habit: 0 points

Example:

Amit started SIPs in diversified mutual funds and gold ETFs, investing ₹10,000 monthly without stopping even in market dips – 10 points.

Neha invests sporadically, often missing payments – 4 points.

Risk Management (Insurance) (0 – 10 points)

Having adequate insurance protects your finances from unexpected risks.

Has comprehensive health and term life insurance aligned with needs, no overlaps: 10 points

Has one type of insurance or inadequate coverage: 5-7 points

No insurance or inadequate coverage: 0-3 points

Example:

Kiran holds health insurance covering ₹5 lakhs and term life insurance with ₹50 lakhs cover – 10 points.

Sameer has no insurance at all – 0 points.

Financial Goals Planning (0 – 10 points)

Score yourself on clarity and planning of financial goals.

Clearly defined short, mid, and long-term goals + mapped monthly savings/investments + regular reviews: 10 points

Goals defined but irregular reviews or planning: 6-8 points

Vague goals with minimal planning: 3-5 points

No goals or plans: 0 points

Example:

Priya has goals for buying a house, a car, and retirement, with quarterly reviews – 10 points.

Aditya is unsure what he wants financially – 2 points.

Spending Pattern (0 – 10 points)

How disciplined are you with spending? Avoid impulse buys, use discounts, monitor subscriptions, live below means?

Consistently avoids impulse buying, optimizes expenses, lives below means: 10 points

Occasional impulse spends but manages overall well: 6-8 points

Regular impulse buying, struggling to control expenses: 3-5 points

Overspending frequently: 0-2 points

Example:

Simran controls spending strictly, monitors app subscriptions, and uses cashback offers wisely – 10 points.

Raj frequently indulges in impulse shopping and OTT subscriptions – 3 points.

Credit Score Awareness (0 – 10 points)

Awareness and management of credit score is another dimension.

Knows score, checks yearly, avoids late payments, keeps utilization <30%: 10 points

Checks credit score irregularly, some late payments: 6-8 points

Rarely checks, poor credit usage: 0-5 points

Example:

Madhuri checks her TransUnion CIBIL score annually, maintains 25% utilization – 10 points.

Vikram is unaware of credit scores altogether – 0 points.

Net Worth Tracking (0 – 10 points)

Do you track your assets and liabilities? Regular updates help monitor wealth-building progress.

Tracks monthly/quarterly, understands net worth trends: 10 points

Tracks irregularly: 5-7 points

No tracking: 0 points

Example:

Rahul calculates net worth quarterly using a spreadsheet, including investments and loans – 10 points.

Neha doesn’t track assets or liabilities – 0 points.

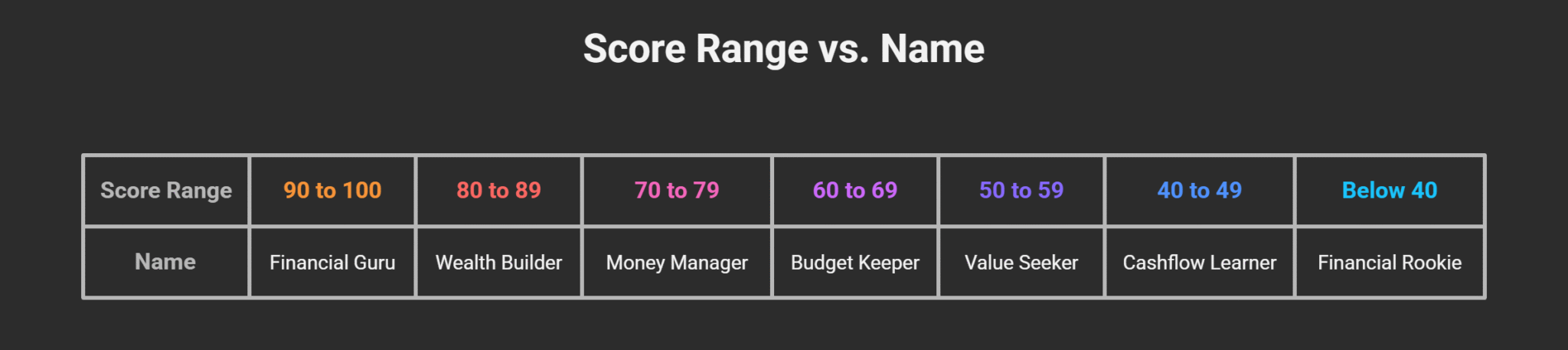

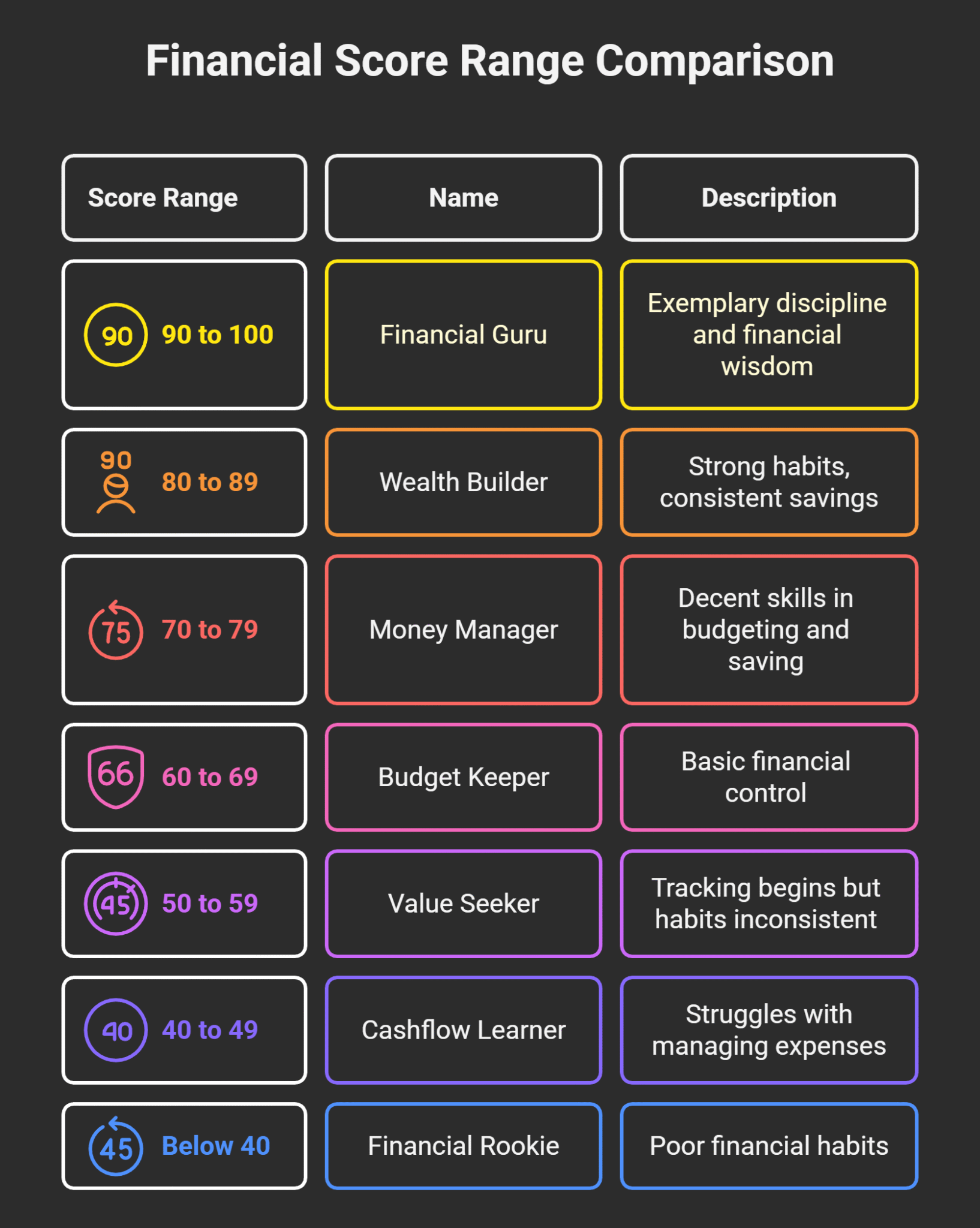

What Does Your Score Mean?

Add up your scores for all ten parameters. Here’s the meaning:

Why Use This Score?

Taking a cold, objective look at your financial discipline score is an eye-opener. It highlights which areas to work on – whether it’s starting an emergency fund, paying debts timely, tracking expenses better, or buying adequate insurance. With this simple self-check, you can set actionable goals to fix your financial mistakes one step at a time.

Final Thoughts

Financial discipline is not an overnight achievement, but a journey. Use this scoring guide as your compass. Regularly reassess your score every 6-12 months, track improvements, and celebrate small wins.

Remember, in India’s growing but volatile financial landscape, being disciplined today paves the way for a secure, prosperous tomorrow.

If you want, you can share your calculated Financial Discipline Score, and the areas you’d like help improving! This score is your first step toward mastery over your money.