Why Lend When Risks Are So High?

Ever wondered how banks make profits by providing loans that carry a huge risk of default, prepayment, credit risk & so on? Yet, banks still encourage taking loans, whether for a home, a vehicle, or a personal loan. Out of 100, approximately 5 borrowers tend to default on the loan that has been sanctioned.

You may wonder that the source of income is through interest received over time, but that would mean the bank would have to deal with interest rate risk, liquidity risk, & constant risk of default; unfortunately, that is not the case.

So, what is it that they do that we haven’t yet been able to decrypt?

Turning Illiquid Loans Into Tradable Assets

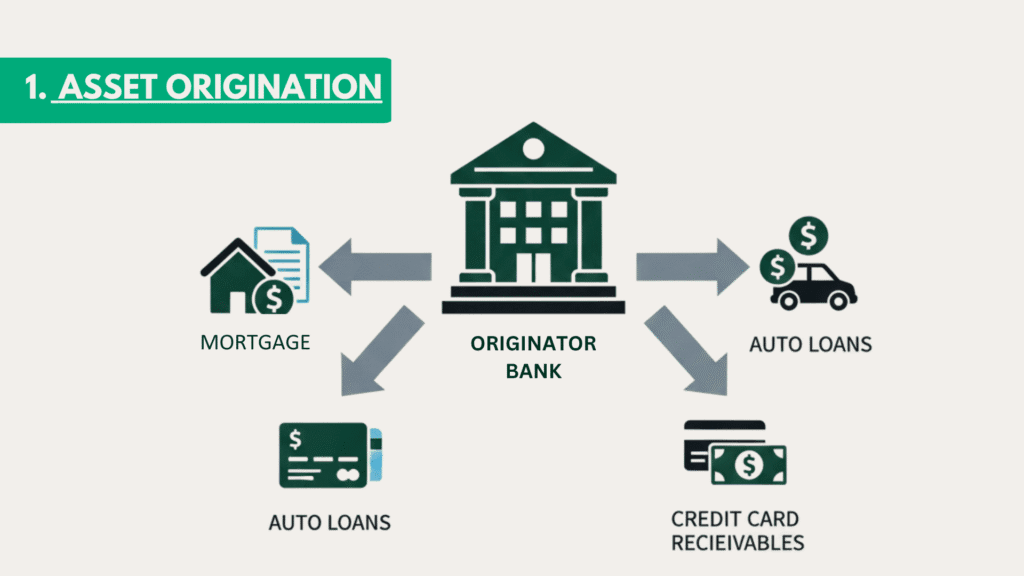

Firstly, banks here are in the business of lending money; the more they lend, the more profitable they are. Certainly, loans are an asset for the banks, but an “illiquid” asset as the loans would be lying idle until it’s maturity.

These big corporations explored how they could make an illiquid asset liquid.

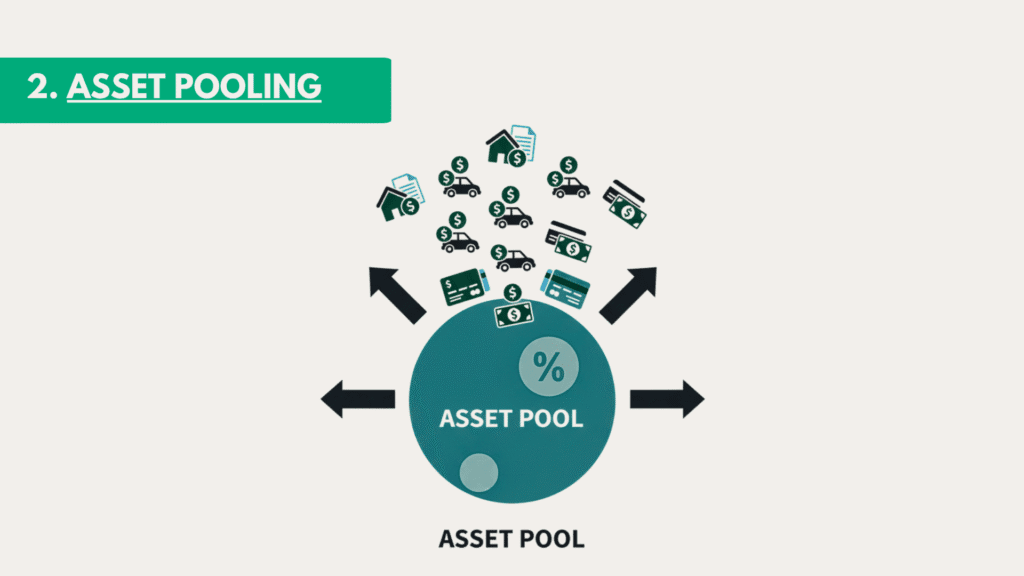

They saw this gap in the market & came up with “securitisation”. In market parlance, this means taking several different loans (untradable) and combining them into one cohesive, tradable security, providing investors with an opportunity to earn through principal and interest payments.

How SPVs Turn Loans Into Investor-Ready Securities

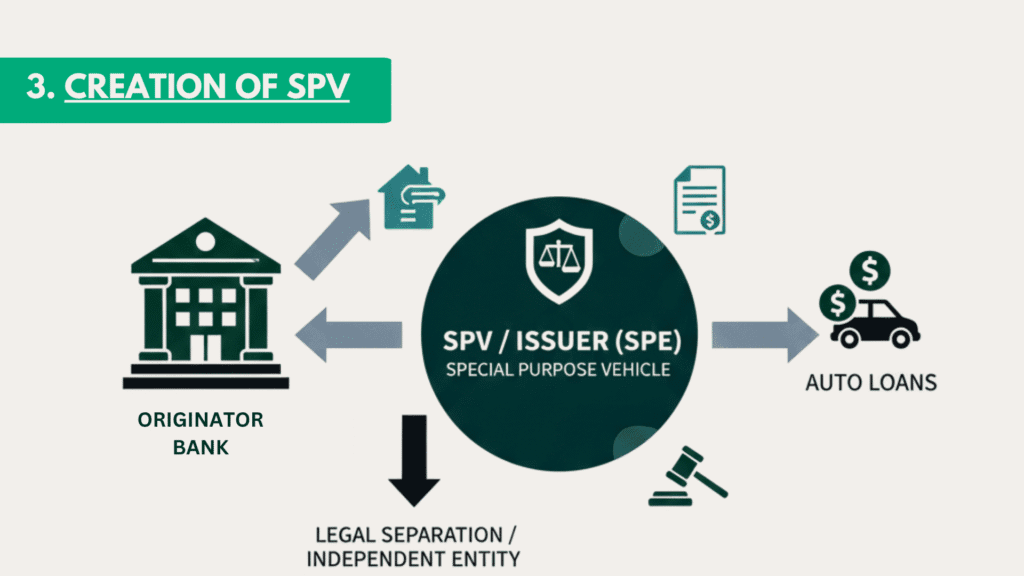

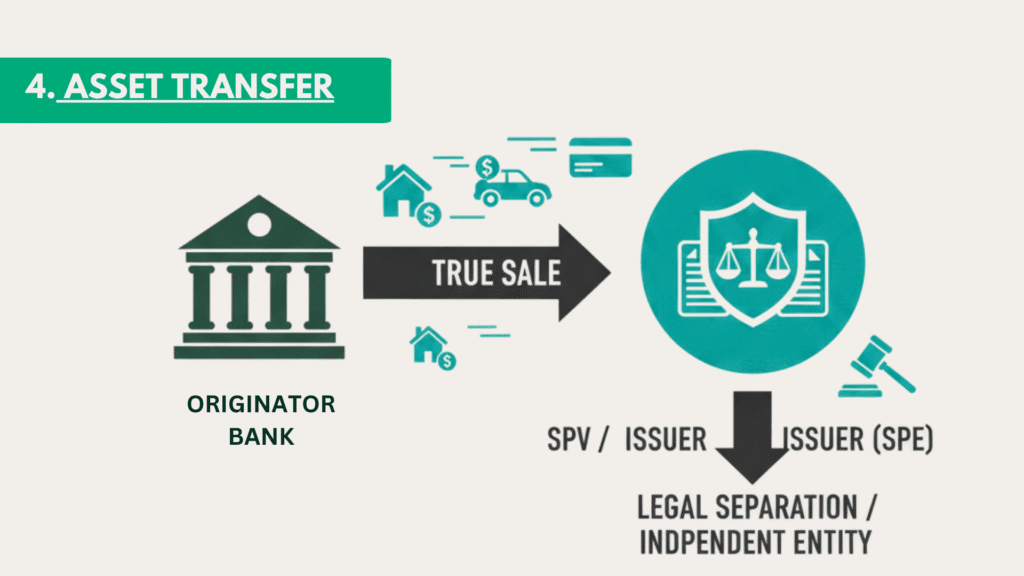

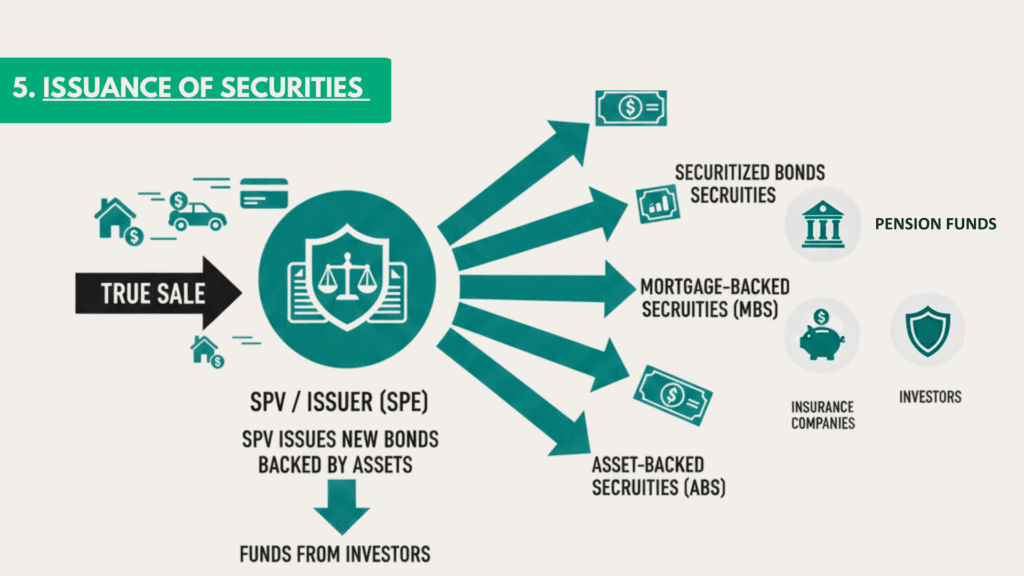

Here, the bank is said to be the originator of this security ( someone who initiated this process). These banks open a trust called SPV or SPE(Special Purpose Vehicle or Entity), a separate legal holding company. Right here, the process starts getting interesting. Now, the bank sells the cohesive loans to the SPV on credit.

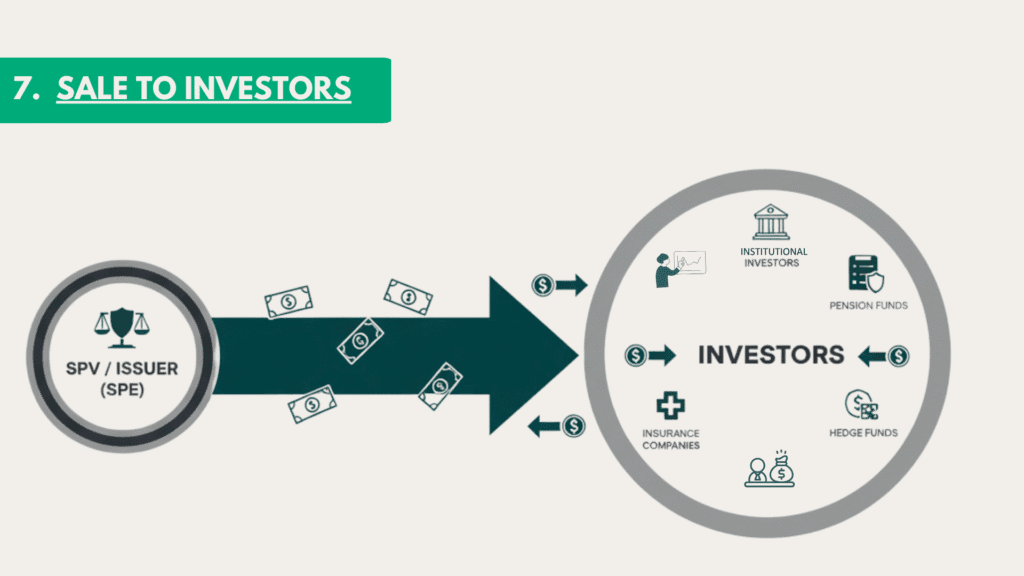

SPV would now issue bonds to investors seeking exposure to such loans.

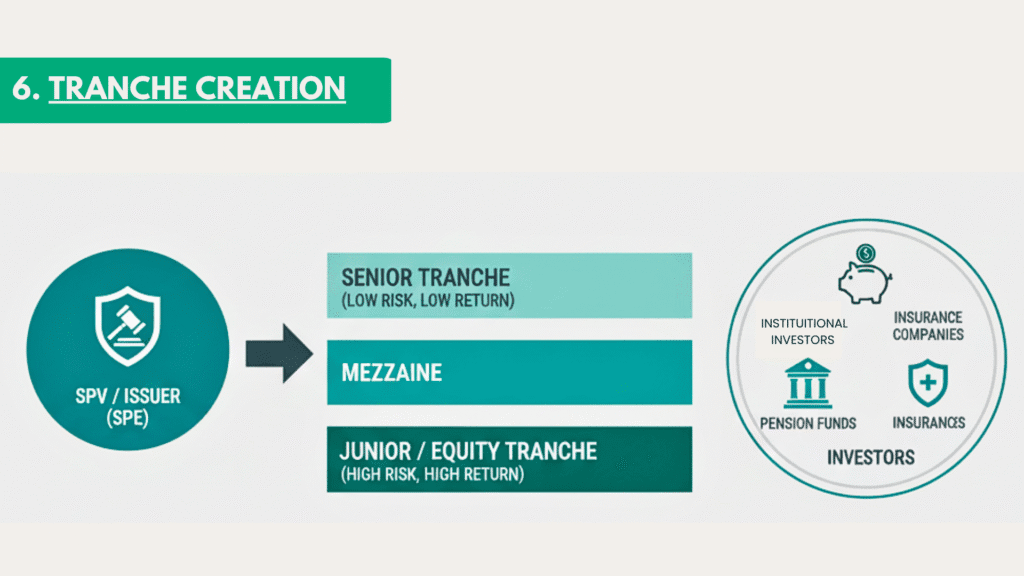

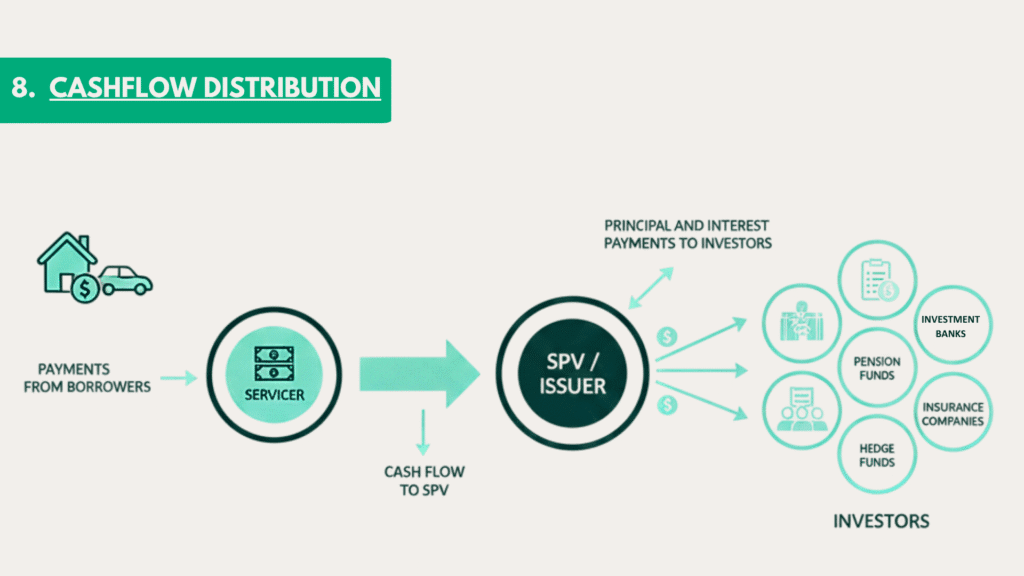

Investors who have purchased the bonds are now funding the loan sanctioned by the bank, but with great returns (principal and interest payments) comes great risk, enabling investors to absorb default & prepayment risks proportionately among investors. With this, SPV transfers the sanctioned loans back to the bank, which it collected from investors through bond issuance.

The Profit Loop: How Banks Earn Without Holding the Risk

Yet, one question remains unanswered: ” How do banks make money out of this process?”

They make money by charging service spreads, which include underwriting, diversification process, creation of loans, and administrative and monitoring costs of the loans that are sanctioned, which is a substantial amount. Essentially, the bank has turned this into a servicing business.

Unfortunately, the banks are not done just yet. The primary way banks make money is by re-issuing the loan they received from the SPV and then restarting the entire process, thus creating a continuous loop.

Final Thoughts

In summary, banks have mastered the art of turning risky, illiquid loans into profitable assets without holding most of the risk themselves. Through securitisation, banks convert lending into a recurring, service-made model while passing credit and prepayment risks to investors. What looks risky to outsiders is, in fact, a profitable business for banks, which allows them to lend more, earn more, and keep the profit loop running.