RBI Rate Cut: Today, Friday, December 5, 2025, the Reserve Bank of India (RBI) made its monetary policy announcement. The repo rate decision was made today after the Monetary Policy Committee (MPC), led by RBI Governor Sanjay Malhotra, convened its fifth bi-monthly meeting for FY26 from December 3 to December 5.

RBI Policy Outcome

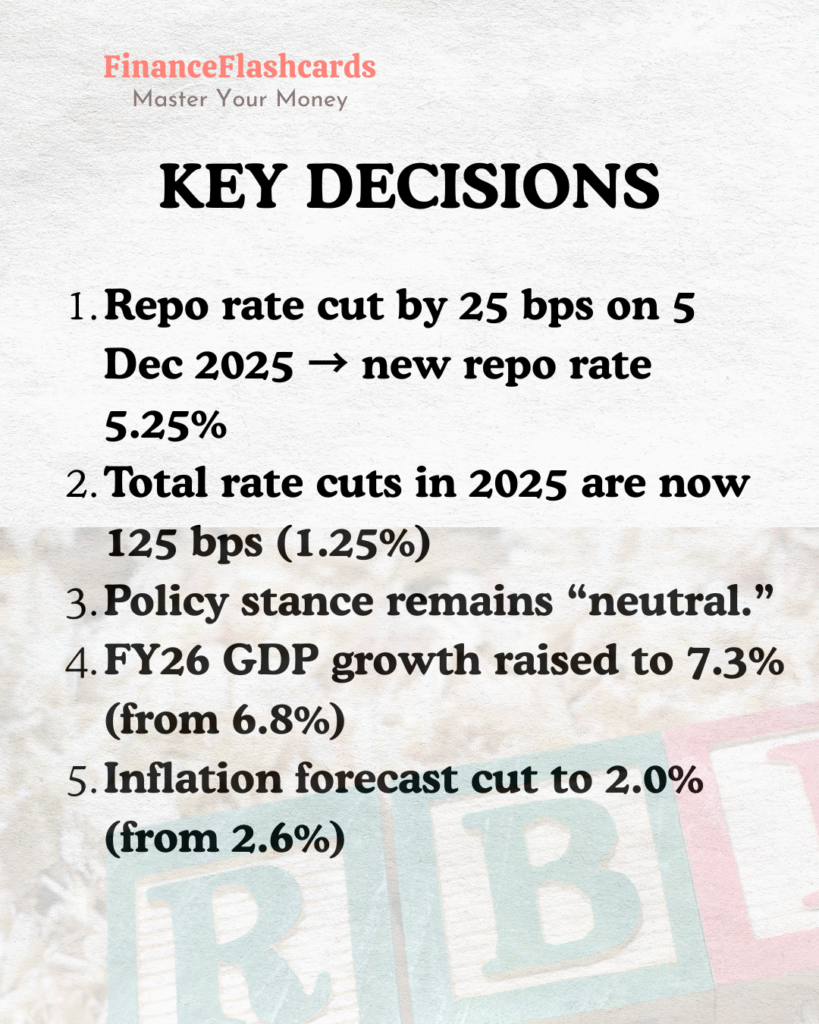

The six-member Monetary Policy Committee (MPC) of the Reserve Bank of India unanimously opted to maintain a “neutral” position and lower the repo rate by 25 basis points, from 5.50% to 5.25%.

Additionally, the RBI increased its projections for FY26 GDP growth from 6.8% to 7.3%. The CPI inflation prediction for FY26 was lowered from 2.6% to 2%. The central bank made the decision to buy ₹1 lakh crore worth of government securities through open market operations (OMO) and to engage in $5 billion in three-year USD/INR buy-sell swaps in December in order to add liquidity to the banking sector.

The RBI reduced the repo rate by a total of 125 basis points in CY 2025. RBI’s 25 bps rate cut draws positive response from market participants

Explaining the rationale behind the rate cut, the RBI governor said, “The growth-inflation balance, especially the benign inflation outlook on both headline and core, continues to provide the policy space to support the growth momentum.”

Impact on Loans: Cheaper but With Conditions

A rate cut means loans will be cheaper as the bank’s cost of funds will fall. That tends to lead banks to lower interest rates on retail and corporate loans — including home loans, car loans, business loans, etc. Borrowers are likely to see reduced EMIs or lower interest outgo if their loans are linked to floating benchmarks.

Now, lower borrowing costs plus greater liquidity encourage households and businesses to borrow, spend, and invest. This can create a demand boost across sectors — real estate, autos, consumer goods, and industrial investment.

As lending rates drop, banks often lower deposit and fixed-deposit rates. That is bad news for savers who rely on interest income (senior citizens, conservative investors), making debt instruments or fixed deposits less attractive.

Impact on Currency (Rupee) & External Flows

As the rupee hit a record low of near ₹ 90+ per USD, the rate cut can further depreciate the Indian currency. The liquidity injection — especially via USD/INR swap — aims in part to manage liquidity and reduce pressure on currency, but a rate cut generally reduces foreign-investor return on Indian bonds/ assets, which can trigger capital outflows, as we have already seen in FY25 that huge capital outflow led to depreciation of the currency.

Rupee may remain under pressure — weakening or volatile — depending on global flows, oil prices, and investor sentiment; this could make imports (especially fuel, electronics, machinery) more expensive.

At the same time, a weaker rupee could help exporters — they’d get more rupees for each dollar earned, potentially boosting export competitiveness.

Impact on Inflation, Economy & Markets

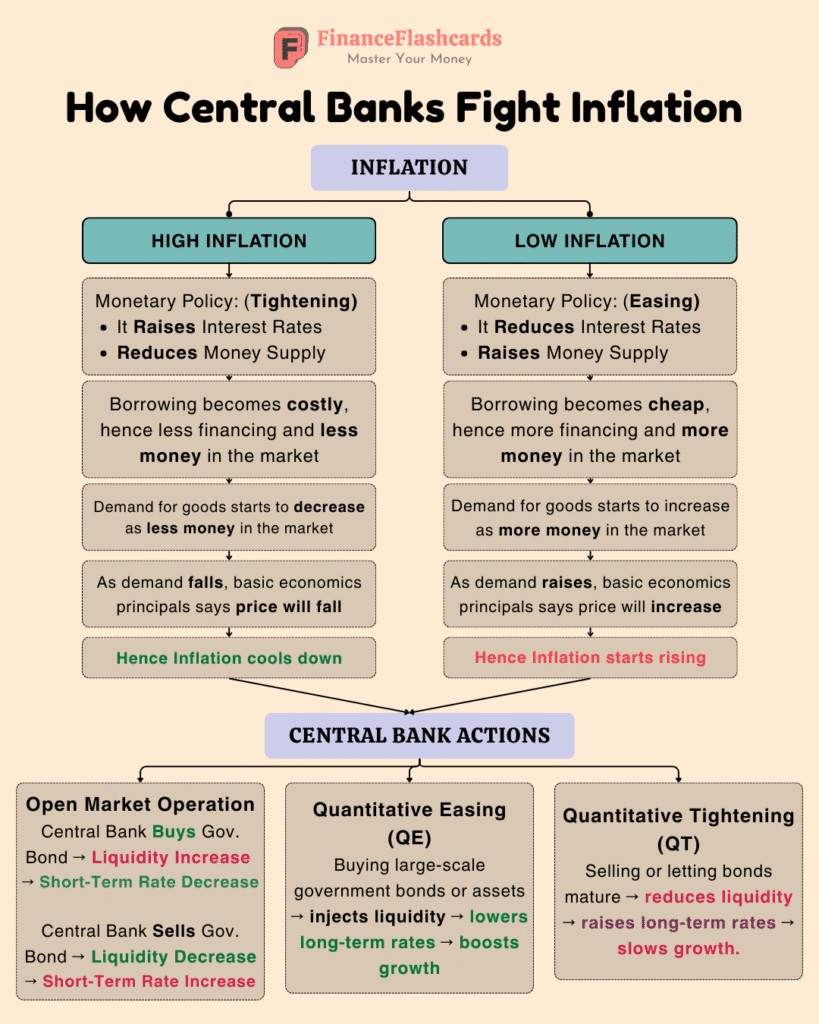

As the rate becomes lower and borrowing becomes cheaper, we see demand-led inflation. If supply doesn’t keep pace, prices may rise — especially in sectors like real estate, automobiles, and consumer goods. Prior research on repo-rate cuts indicates such moves tend to raise inflationary pressures if demand ramps up.

With growth forecast raised (7.3% for FY26), sectors like housing, infrastructure, auto, consumer goods, and services are likely to get a boost. Lower borrowing costs and better credit transmission will help businesses expand operations.

If credit growth surges without a commensurate rise in supply of goods/services, inflation may pick up. This could force RBI to reverse course later.

The Bottom Line

Given that inflation is currently in the target range and growth momentum is strong, RBI’s decision to cut repo rate — along with deploying liquidity tools (OMOs, forex-swap) — appears to be a deliberate, growth-supportive move. It aims to boost demand, credit flow, investment and consumption.

If managed carefully, with stable currency and steady supply-side response, this could help sustain India’s growth without triggering runaway inflation. But much depends on how banks respond, how domestic and global conditions evolve — inflation, currency, capital flows.