Definition and Core Characteristics:

A Hedge Fund is a private collective investment fund that is created with the intention of earning an absolute return or risk adjusted. They are managed by an investment firm that is organized as a private limited company (an LLC or as a partnership) and they are restricted to accredited investors only. Since hedge funds are subject to very little regulation, they are able to employ a number of different strategies including leverage, derivatives and short selling without the same restrictions that are placed on a mutual fund. Common fee structures for hedge funds include a management fee of 1-2% of assets + incentive fees (20% of profits), as well as being allowed to invest in other securitized assets (i.e.: bonds, commodities, cash, foreign exchange, complex derivatives) and illiquid assets, such as distressed debt and private equity. On average, the fees for a hedge fund (a management fee of 1-2% and an incentive fee of 20%) are usually based on a two-tiered fee structure.

Key characteristics of Hedge Funds include:

- Eligible Investors: Hedge funds are exclusive investments available only to experienced, high-net-worth or institutional investors who are considered “accredited” or “qualified purchasers.”

- Regulatory Typology: Hedge funds do not have to comply with most of the requirements of the Securities Act of 1933 by being established as “private” funds with no registration, or by operating under one of two exempt statutes: the securities laws created under Section 3(c)(1) or Section 3(c)(7) of the Investment Company Act of 1940. Hedge funds aren’t required to publish daily statements of their NAV or holdings, are not subject to mandatory redemption rights, and may use unlimited amount of leverage or shorting.

- Flexible Tools: In order to execute their strategies, hedge funds use substantial amounts of leveraged and short selling, and derivatives. In addition, hedge funds may hold illiquid investments (e.g. distressed debt or investments in private public companies) in order to increase their perceived returns.

- Management Structure: Hedge funds are usually established on a “fund” model where the fund is an investment pool (as a limited partner) and the management company or general partner provides investment and general fund management. This model, in conjunction with the other services that hedge funds utilize (e.g. administrators, prime brokers, custodians and auditors), provides multiple levels of oversight.

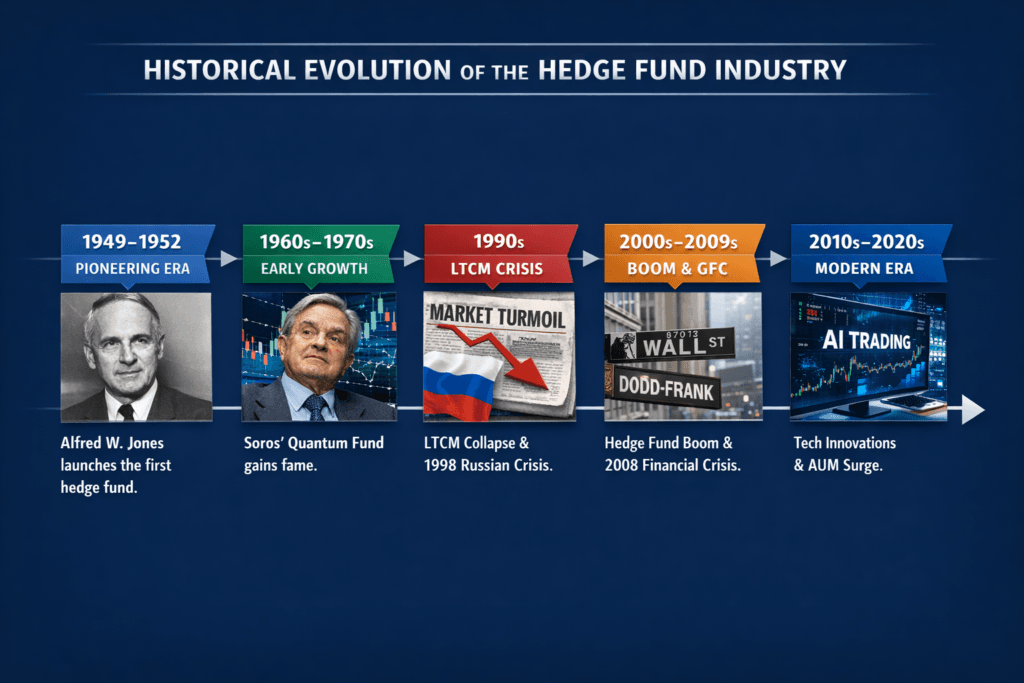

Historical Evolution of the Hedge Fund Industry:

Hedge funds, as a financial vehicle, first appeared on the investing landscape in 1949 with Alfred Winslow Jones’ establishment of the first long/short equity fund. Moreover, Jones introduced the concept of using the limited partnership structure and having a separate performance fee for investors and managers. These two fund-structuring innovations are fundamental to what we now refer to as hedge funds. The timeline of hedge fund development is characterized by, among other events, several significant milestones:

1949-1952: Alfred W. Jones developed and operated the first hedge fund. His approach was to take both long and short positions in stocks to decouple the manager’s skill from the market’s movements. In 1952, he formalized the use of a limited partnership structure and performance fee.

1960s-1970s: The rapid growth of hedge funds resulted from increasing media coverage about the exceptional long-term performance of Jones’ fund. In 1969 George Soros’ Quantum Fund generated spectacular returns using a global macro strategy and significantly increased the profile of hedge funds among wealthy investors, but the total number of hedge funds was still small.

1990s: The introduction of institutional investors, particularly endowments and pension funds, into hedge funds provided for a sizeable increase in hedge fund assets. However, many issues arose during this period that had significant impact on hedge fund managers and investors. The most notable was the collapse of the highly leveraged arbitrage fund Long-Term Capital Management (LTCM) in 1998 during the Russian debt crisis. The near-collapse of LTCM and its subsequent, government-supported $3.6 billion bailout by major banks demonstrated the systemic risk created by using significant amounts of leverage in hedge fund strategies.

2000s: The hedge fund industry saw a sharp increase in growth during the early 2000’s, however the industry suffered a decline in 2008 through 2009 with many funds closing or merging after the global financial crisis. The era after the crisis saw many regulatory shifts (Dodd-Frank by requiring many large hedge fund managers to register with the Securities and Exchange Commission), but also allowed for new strategies to be developed that leverage technology.

2010s – 2020s: After 2008, hedge funds began to recover from a reduction in AUM with a renewed focus on more sophisticated risk management. By 2024-2025, the hedge fund industry is expected to have several trillion in total AUM globally. Recent years have seen significant inflow and assets; In Q3 of 2025 hedge funds are expected to hold nearly $5 trillion due in part from a high volatility environment and an increase in the use of new strategies.

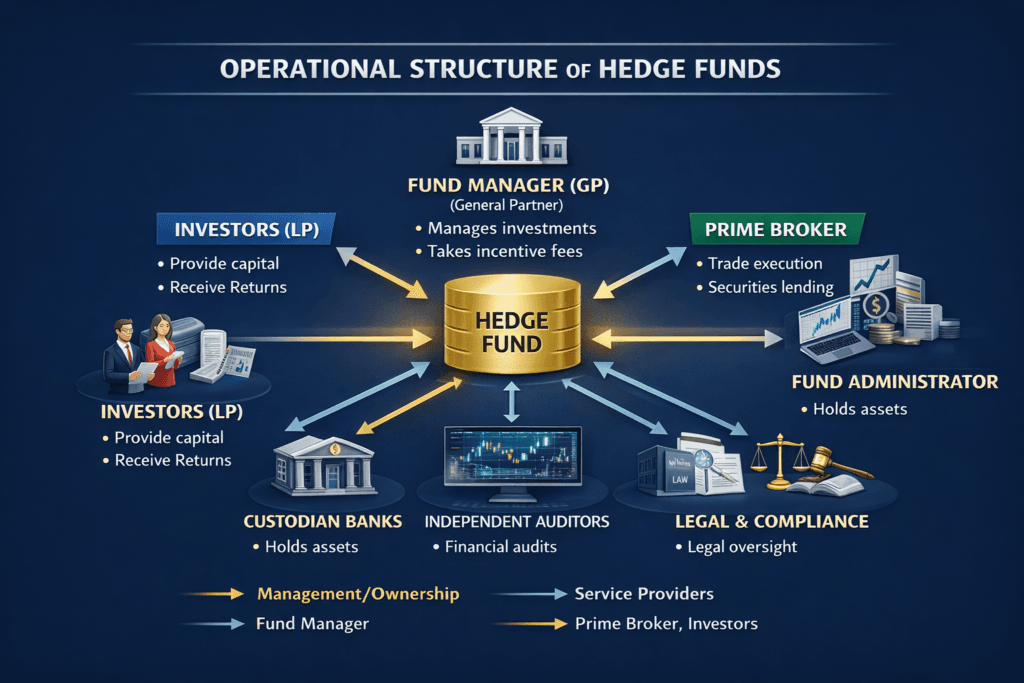

Legal and Operational Structure:

Limited Partnerships (LP) or LLC’s are generally used by hedge funds for their legal structure in establishing the fund entity. The fund entity serves as the investment vehicle with investors being limited partners. The manager, typically an LLC created for this purpose, serves as the fund’s general partner (i.e., administers the fund and has fiduciary responsibilities to investors). The General Partner (GP) is responsible for executing all trades and is typically assisted by analysts and portfolio managers. The separation of the fund and GP gives limitations on liability of the GP and creates clear reasons for distribution of management fees. Hedge funds are private placements and have relied on SEC exemptions under §3(c)(1) or §3(c)(7) to avoid registering with the SEC as investment companies by limiting the number of accredited or qualified individuals”

Providers of Services: The hedge fund has a great deal of middle office and back office obligations that they usually contract out to other providers. Most funds will use a prime broker for executing securities trades and financing the purchase of those securities (through a combination of securities lending, leverage, or possession of liquid assets). An independent fund administrator will establish Net Asset Value (NAV) and process subscriptions and redemptions of shares along with providing the investor with required reports. Banks that serve as custodians will maintain the cash and the funds’ assets and, for many funds, the prime broker is the custodian of their liquid securities. In addition, external auditors and attorneys will perform audits of the financials of the fund, reviews for compliance with applicable laws and regulations, and perform legal work related to the organization of the fund. This multi-layered arrangement (GP vs Fund vs Independent Administrator) provides additional checks and balances. In particular, by utilizing independent fund administrators and auditors, the fund receives 3rd party objectivity and additional protection from operational risk.

Regulatory status: The hedge fund management company may be regulated (for example, large managers may need to register as investment advisers and comply with anti-money laundering laws), but the hedge fund itself is largely exempt from the provisions of the 1940 Act. In contrast to mutual funds, hedge funds are not required to calculate their net asset value (NAV) on a daily basis or allow redemption of shares on a daily basis, and there are no limits placed on the amount of diversification or leverage that hedge funds can utilize. As a result, hedge funds can only be sold to accredited investors through a private placement.

Investment Strategies and Tools:

There are different types of hedge funds with their own different strategies, and some hedge funds could be combined.

- A standard long or short equity is the strategy where the fund manager purchases stock in companies the manager believes are undervalued and sells stocks in companies that the manager believes are overvalued in an attempt to earn money through their stock selection skills, and hedge some of their overall exposure to the overall market.

- Market-neutral or statistical arbitrage, both of which are forms of equity strategies, are utilized by the portfolio manager to have equal long and short market exposure in order to isolate “alpha,” i.e. their excess return performance separate from overall market movements, which are typically found in strategies such as dollar-neutral equity arbitrage or pairs trading.

- The Global Macro strategy allows the hedge fund manager to employ both “macro” and “micro” investment philosophies by making trade decisions based on their macroeconomic outlooks and expectations, and also by accumulating sufficient positions in currencies, interest rates, stock indexes, and commodity markets. Some examples of macro strategies include using futures to express economic views and trading options on stock and commodity indexes.

- Event-driven funds tend to focus on investing based on corporate events, such as merger arbitrage (buying stock in target company and selling stock in acquiring company), distressed investing (investing in debt instruments of companies experiencing financial challenges), activism (investing to effect change at a targeted public company), and special situations (spin-offs, asset restructurings).

- Relative-value fixed income arbitrage strategies typically connote taking advantage of differing parts of the same yield curve or taking advantage of discrepancies in the valuation of bonds or credit (for example, a convergence trade among government bonds as opposed to mortgage backed securities or convertible bonds), and are often leveraged to maximize a relatively small pricing inefficiency.

Examples of systematic, quantitative hedge fund strategies include statistical arbitrage, quantitative investing, and algorithmic trading. For these funds, the decision-making process involves the use of statistical signals to execute trades across a multitude of different financial instruments. An example is using statistical indicators to create a model to trade stock index futures; this model generates data that can be analysed to help determine potential future price movements in any equity security. Typically included in these models are price trends, volatility patterns, correlations between asset classes, and fundamental valuation measures.

Some hedge funds utilize multiple strategies within their organization, while others focus solely on systematic absolute return strategies; these funds may trade futures contracts on behalf of their clients, known as managed futures funds or commodity trading advisors (CTAs).

Within the context of hedge fund investment strategy, many hedge funds employ the following three investment techniques: short selling (borrowing and selling an asset that is expected to decline in value), leverage (borrowing money from a broker), and derivatives (options, swaps, etc.) to achieve a desired return.

A classic example of one of the aforementioned strategies is: a hedge fund purchases shares of convertible debt, then hedges its short position against the underlying common stock. Subsequently, the hedge fund seeks to capitalize on the mispricing between the convertible debt, the conversion feature embedded in the convertible debt, and the price of the underlying equity security.

Conclusion:

Hedge funds are a subsidiary of the financial field, and offer a very flexible & highly complex form of investment. Hedge Funds are supposed to produce an absolute (as well as relative or adjusted) return on investment by primarily using many different types of Investments both normal and unconventional. Hedge Funds are subject to very few regulations which provide a lack of restrictions, or regulations will permit the use of more sophisticated techniques; such as: leverage; derivatives (options and futures); short sales; etc. This flexibility can potentially produce increasing returns, and increased diversification; however it has the potential for much greater risks than either traditional or non-traditional means of achieving investment returns. In other words, the potential risk of hedge fund investments are mainly related to leverage, liquidity and transparency issues. Therefore hedge funds should only be appropriate for accredited investors who possess adequate experience, knowledge and risk tolerance to adequately evaluate and make sound investment decisions about hedge funds and other types of investments.

Bibliography:

- Securities and Exchange Commission. Investment Company Act of 1940. U.S. Government Printing Office, Washington, D.C.

- Securities and Exchange Commission. Investment Advisers Act of 1940. U.S. Government Printing Office, Washington, D.C.

- Hedge Fund Research, Inc. Global Hedge Fund Industry Report. Hedge Fund Research Publications, Various Years.

- Dalio, Ray. Principles: Life and Work. Simon & Schuster, 2017.

- Lowenstein, Roger. When Genius Failed: The Rise and fall of Long-Term Capital Management. Random House, 2000.

- Mallaby, Sebastian. More Money than God: Hedge Funds and the Making of a New Elite. Penguin Press, 2010.

- Simons, Jim. “Quantitative Trading and Market Efficiency.” Journal of Portfolio Management, Various Issues.

- Fabozzi, Frank J. Fixed Income Analysis. CFA Institute Investment Series, Wiley, Latest Edition.

- Bodie, Zvi; Kane, Alex; Marcus, Alan J. Investments. McGraw-Hill Education, Latest Edition.

- Global Hedge Fund Assets and Performance Reports. Reuters Financial News Service, 2022–2025.

- Hedge Fund Industry Insights and Performance Analysis. Bloomberg Professional Services.

- CFA Institute. Alternative Investments. CFA Institute Curriculum, Level II & III Readings.

- Malkiel, Burton G., and Atanu Saha. “Hedge Funds: Risk and Return.” Financial Analysts Journal, CFA Institute.

- S. Department of the Treasury. Systemic Risk and Hedge Fund Oversight Reports. Washington, D.C.