Hey there readers.

Welcome to this special edition on Global Economics, where we understand and analyze the ‘Yen Carry Trade’, and how this could shape global currency flow dynamics in 2026, amid easing global trade frictions. Even as concerns linger over Japan’s long term fiscal health, especially after the historic victory of Prime Minister Sanae Takaichi in the recent snap elections held in the country (reported in our daily market edition on February 9, 2026).

We get underway by taking a look at the Bank of Japan’s (BoJ’s) recent monetary policy stance before we get to the Yen carry trade.

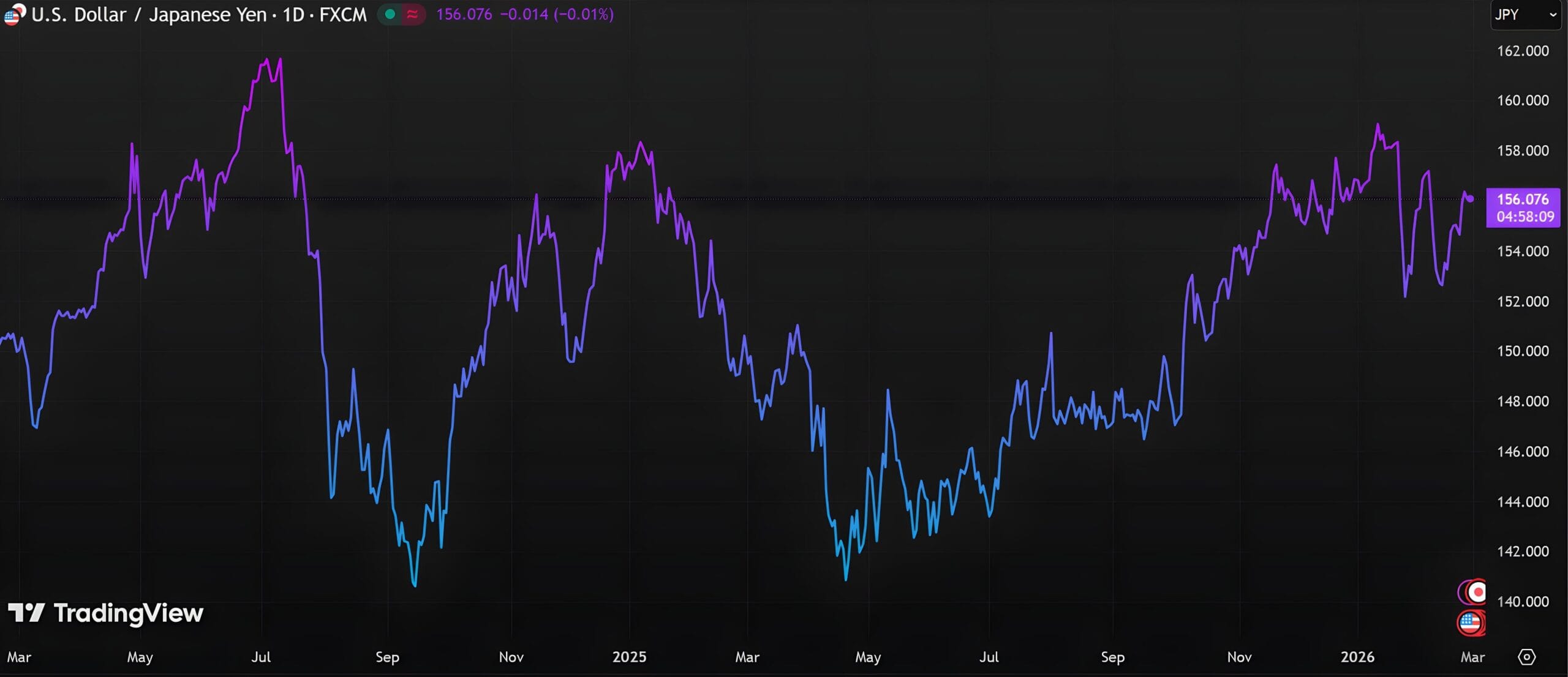

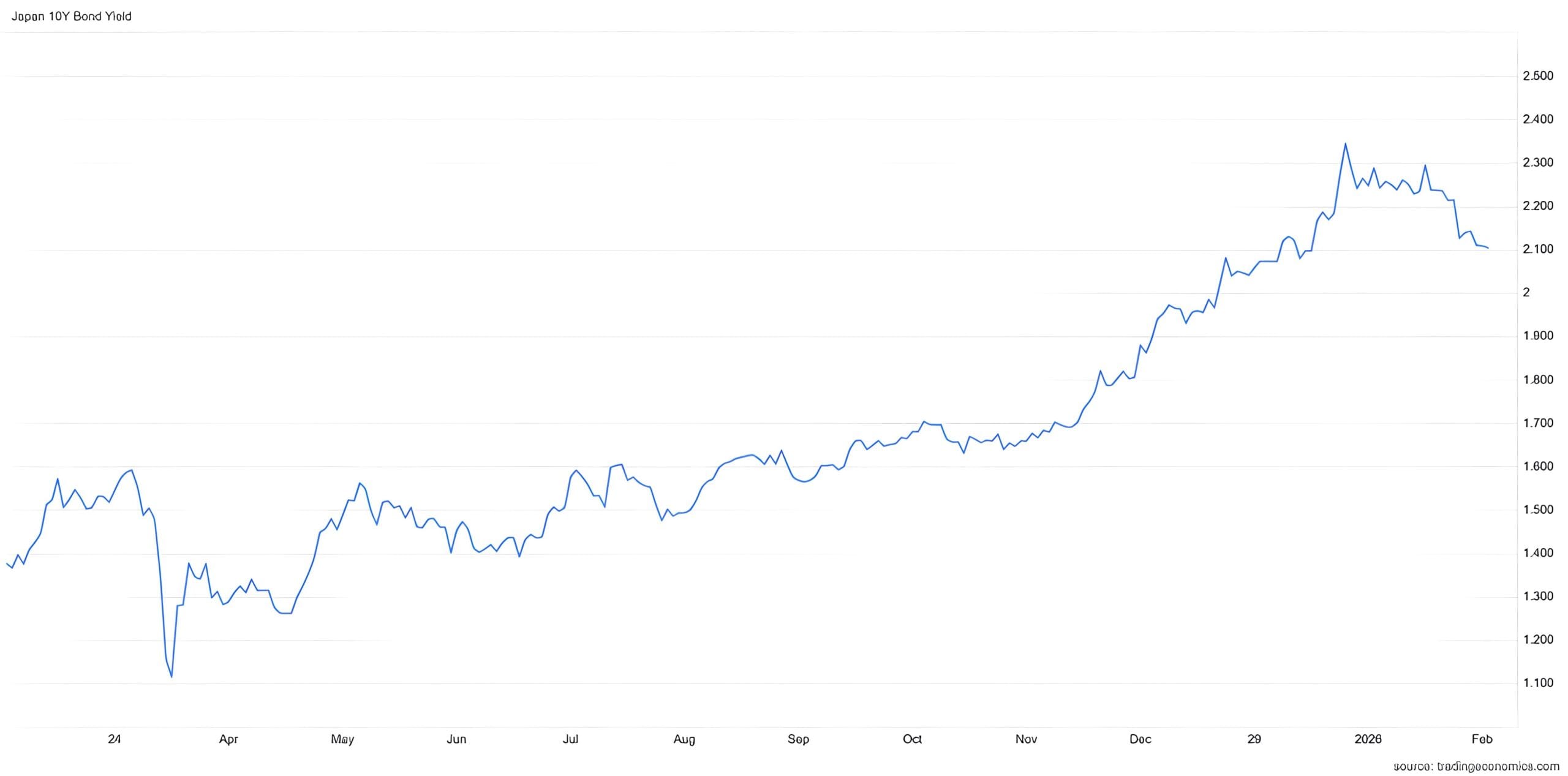

The Bank of Japan (BoJ) is expected to continue its gradual policy normalization, rather than aggressive tightening, after the interest rates were raised by a quarter point to 0.75% in December, the highest level in three decades. Supported by steady 3-4% nominal growth and persistent inflation concerns since 2022, markets are increasingly pricing in additional policy adjustments, with expectations of multiple hikes in 2026. This evolving policy trajectory has drawn renewed global investor attention, bringing the next unwinding of the Yen Carry Trade – a strategy built on and entailed by cheap yen borrowing, back into the spotlight.

What is the Yen carry trade?

For years, investors borrowed the Japanese yen at exceptionally low costs enabled by BoJ’s policy of near-zero and negative interest rates. This capital was converted into foreign currencies and deployed to build leveraged positions in higher-yielding assets across the globe – from US bonds to EM equities – to capture the wider yield spreads. Higher interest rate differentials (IRDs – The difference in bond yields between two countries) alongside a weak yen ensured the trade worked best, with such a low cost borrowing environment translating into higher investor returns as this ‘carry’, often amplified with leverage.

Japan’s fiscal outlook

The yen remained structurally weak for years as the markets refrained from pricing in rate hikes aggressive enough to drive meaningful currency appreciation. This left BoJ Governor Kazuo Ueda navigating a complex policy trade-off, balancing policy tightening against inflationary and long-term fiscal sustainability concerns. A late-January sell-off in the benchmark 10-year Japanese Government Bonds (JGBs) pushed the yield to 2.38% — a 27-year high — signalling shifting market expectations around Japan’s policy trajectory.

As the central bank reassesses its stance, the risk of a broader unwind of the leveraged carry positions could begin to reshape capital and currency flow dynamics in 2026. The carry trade had been long anchored on wide interest rate gaps (favorable IRDs) between Japan and higher-yielding economies, alongside a persistently weak yen, both of which face increasing uncertainty.

What could the unwind mean for EMs including India?

If the yen strengthens and BoJ move toward higher rates in 2026, funding costs for investors with yen-denominated liabilities in the emerging markets (EMs) could rise, after decades of ultra-loose policy. This means higher costs to service the debt, prompting investors to deleverage across carry-funded positions, with global implications. Morgan Stanley estimates suggest roughly $500 billion in outstanding yen-funded carry positions despite the partial unwind last August. That episode reiterated the unwind is not confined to Japan, with the S&P 500 falling 6% over three sessions amid liquidity-driven selling as the Tech stocks underperformed due to carry trade outflows.

For India, where foreign portfolio investor (FPI) flows play a significant role in capital markets, this dynamic could translate into currency volatility from global FX shocks alongside episodic FPI outflows. Bond market positioning may also witness additional adjustments, even as domestic growth and earning expectations continue to anchor medium-term investor interest.

That’s all from me in this edition on the ‘Yen Carry Trade’.

Do share your feedback in the comments below, and Stay curious..

Happy Reading!

PS: If you like the author’s work and contribution to this platform, and wish to discuss more related to Markets and Macroeconomics in particular, do follow and connect with me, or dm me on-

LinkedIn @AnudityaGupttaa