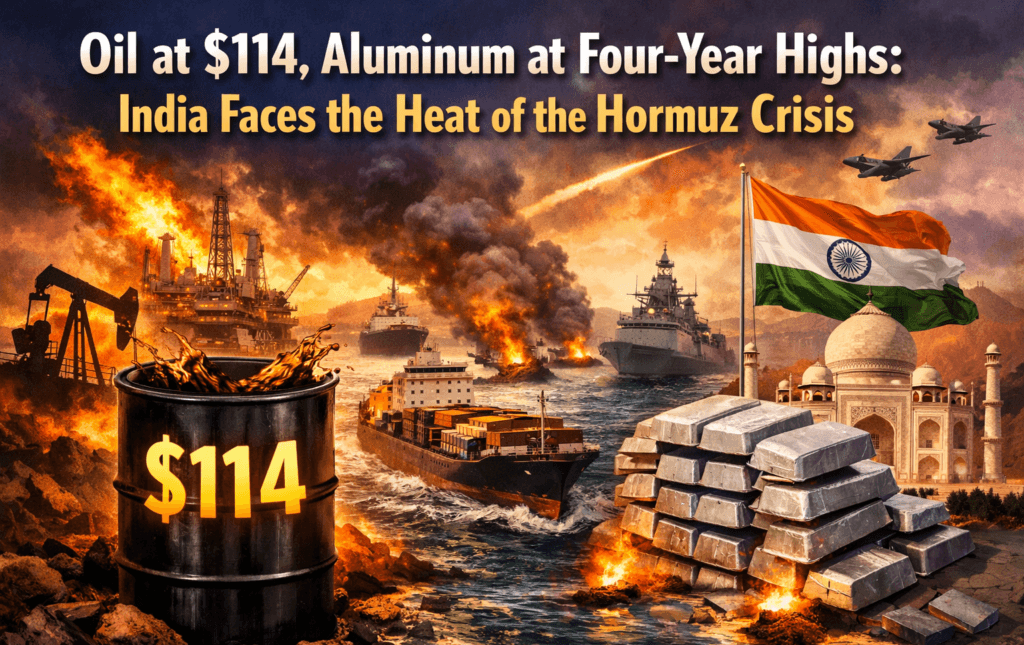

The escalation of the Middle East conflict into a full-blown “Hormuz Crisis” has fundamentally altered the global economic landscape overnight. For India, the world’s third-largest oil importer, the convergence of a physical supply crunch, surging commodity prices, and a flight to safe-haven assets represents a worst-case scenario. Here is an analysis of the developments and their implications for the week ahead.

The Energy Shock: Oil Tests Critical Resistance

The most consequential development is the vertical spike in crude prices. Brent futures surged nearly 23% in early trading, touching a session high of $119.45 per barrel before settling near $114. The move is not merely speculative; it is a direct response to a tangible supply disruption. With Iraq and Kuwait implementing output cuts and the Strait of Hormuz effectively a war zone, the market is pricing in the loss of a significant portion of Middle Eastern spare capacity.

The technical outlook for both Brent and WTI is now “Very Bullish,” suggesting further upside if strikes on Iranian energy infrastructure continue. For context, every sustained $10 increase in oil prices widens India’s current account deficit by approximately 0.4% of GDP. The $120 level for Brent is now a critical threshold; a sustained close above it would likely trigger a secondary wave of selling in global equities as recession risks are repriced.

Metals Join the Rally: Aluminum at Four-Year Highs

The supply shock is not confined to energy. Aluminum surged to its highest level since April 2022, crossing $3,500 per ton. The Persian Gulf accounts for roughly 9% of global aluminum supply, and at least two major smelters in Qatar and Bahrain have suspended deliveries. U.S. buyers are already scrambling for alternative cargoes from Asia.

This adds a new layer of cost-push inflation for industries ranging from automotive to aerospace. For India, a net importer of critical metals, this will exert additional pressure on manufacturing input costs and is likely to reflect in weaker PMI data later in the month.

India’s Economic Siege: Rupee, Bonds, and Equities Under Pressure

For Indian financial markets, the confluence of these global shocks creates a challenging environment across asset classes.

The Rupee: The currency is at risk of breaching the 92.50 per dollar mark. Importers are rushing to hedge future costs, while exporters are delaying dollar conversion, exacerbating the downward pressure. The Reserve Bank of India’s intervention has provided a backstop, but analysts note that the longer the shock persists, the less sustainable this policy becomes.

Government Bonds: The benchmark 10-year yield is under pressure to rise despite the RBI’s massive ₹1 trillion bond purchase programme scheduled for this week. The market’s focus remains on the inflation trajectory, and central bank liquidity operations are viewed as a temporary shield rather than a solution to the underlying macroeconomic deterioration.

Equities: Domestic indices are facing a significant gap-down open, with the GIFT Nifty indicating a volatile and negative session. Markets are pricing in the impact of higher input costs on corporate margins and the broader growth outlook.

The Geopolitical Timeline Driving Markets

Market direction this week will be dictated less by economic data and more by the trajectory of the conflict.

Iranian Leadership: The appointment of Mojtaba Khamenei signals a hardening of the regime’s stance, suggesting a prolonged “war of attrition” rather than a swift de-escalation.

U.S. Policy: Official statements indicating support for strikes on Iranian economic infrastructure point to an expansion of the conflict’s scope.

Supply Chains: Shipping through the Persian Gulf has been effectively paralyzed. Freight rates and insurance premiums are expected to rise sharply, adding further friction to global trade.

Strategic Outlook

This is no longer a localized geopolitical event; it is a global stagflationary shock. Energy and metals are the only asset classes showing strength, but their gains function as a tax on the broader economy. Equities and bonds are in a defensive posture, bracing for earnings downgrades and persistent inflationary pressure.

The key level to monitor is $120 for Brent crude. A sustained breach of this threshold would likely accelerate the repricing of recession risk across global financial markets. For India, the week ahead promises elevated volatility, continued pressure on the rupee, and a highly active Reserve Bank of India working to maintain stability on multiple fronts.