Financialization means an increased percentage of savings by households are transferred to financial instruments versus traditional safe instruments for savings; for example, we see that families are moving away from bank FDs, gold and cash and will invest in stocks, mutual funds, investment-linked products and even private credit. These changes are driven by low rates of return on bank deposits, historically low interest rates – in some cases even below the rate of inflation, and the need for higher-yielding investments. The ability of families to, however, make these investments has been created by technology and structural changes; for example, fintech apps (discount brokerages, robo-advisors) have made it very easy to start investing in equity markets; UPI and other forms of digital payments have made it easy to access OTC cash for investing; and online information platforms provide education and entice new and inexperienced investors. Some new investment product offerings (e.g., SIPs, index funds) allow investors low-cost access to create systematic investment strategies. In addition, the regulatory environment in India, as well as the media, has helped to support and promote market investments. According to Motilal Oswal’s analysis, the increasing participation of families in credit, capital markets and insurance has commonly been referred to as the “financialization of savings” during the post-Covid period, as many new households became active investors between 2021 and 2022 due to Covid-related lockdowns (i.e., Zoom learning), and the amount of individuals that began using free online trading thereafter was significantly enhanced.

On the demand side, there are several changes in customer profiles which include demographic and behavioral profile changes as well. There are more younger investors in India than at any other point (approx. 32 years old for median age by FY2025) and they tend to live in urban areas and are more open to taking risks (or at least are aware of risk). Older savers remain conservative with their investments; however, even retired savers have recently average shifted slightly towards investing in secure debt instruments and balanced investment products. Further behavioral influences include fear of missing out on equity returns, the herd mentality during a bull market, and mutual funds viewed as “safe” long-term investments have also encouraged this shift. Other emerging markets have experienced similar trends, such as the increased encouragement of retail investors in China to invest in stock markets to further diversify their savings by traditional means, and central bank rates decreased due to economic crises in various geographies post-crisis (and subsequently created a more complete” private fund investing universe).

Data & Trends: India and Globally

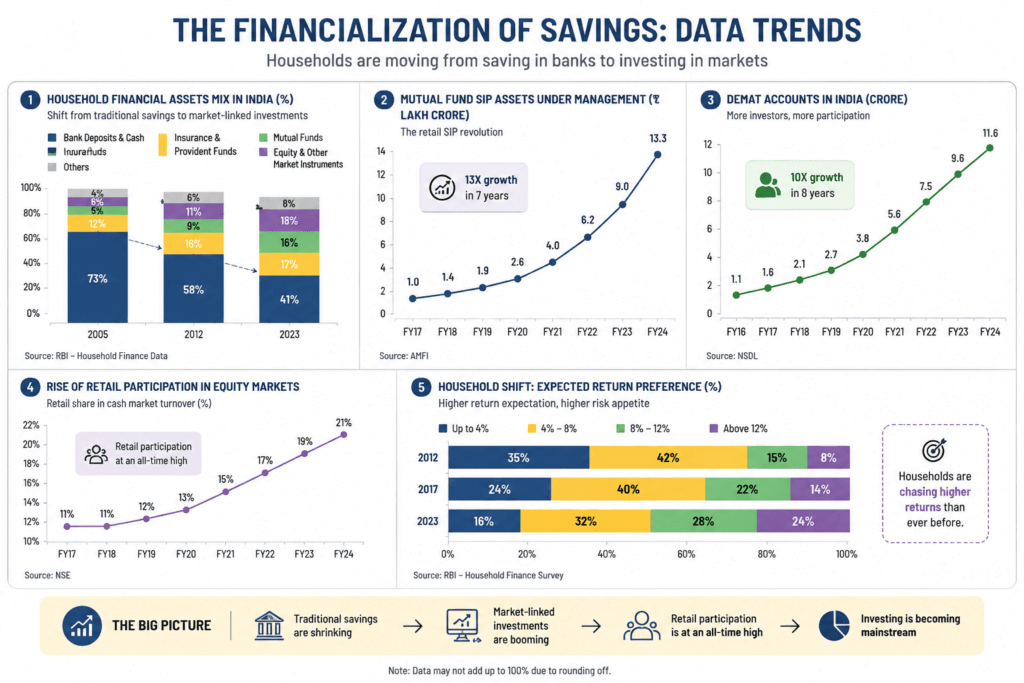

There has been a longstanding shift for Indians into equity and mutual funds using household savings as the vehicle of choice for this reallocation since FY2012. According to the Reserve Bank of India (RBI) estimates and Economic Survey, from FY2012 through FY2025, the amount of net flows from Indian households’ financial savings into equity and mutual funds has grown from approximately 2% to approximately 15%.

As of September 2025, Indian households had increased their investment in equity (directly and indirectly) tenfold (approximately ₹8 lakh crore in FY2014 to approximately ₹84 lakh crore), even though the amount of direct equity ownership had only grown slightly (from approximately 8% of total assets to approximately 9.6%). However, due to the growth of indirect equity ownership through mutual funds, the percentage of total assets represented by indirect equity ownership will have nearly tripled from FY2014 to September 2025 (from approximately 3% to approximately 9.2%).

During the same period, equity savings have represented a smaller share of total financial savings than traditional savings product categories, such as treasury bills and time deposits. The percentage of deposit account holdings to total household financial savings will fall from over fifty-eight percent at the end of FY2012 to approximately thirty-five percent at the end of FY2025. However, despite the reduction in equity as a percentage of financial savings, there are still large amounts of credit-related financial savings (i.e., provident funds, pension funds, and insurance).

As of March 2025, the RBI reported that approximately twenty-three percent of total household financial savings will consist of equity and mutual funds, up from approximately fifteen percent at the end of 2019.

The growth of SIPs is one of India’s biggest enablers. Monthly SIP contributions have risen dramatically from less than ₹4,000 crore in FY2017 to over ₹28,000 crore by FY2026, reflecting huge retail capital inflows. By May 2025, active SIP accounts exceeded 8.5 crore, and total AUM for Indian MFs exceeded ₹70 trillion as of late 2025 (18% CAGR since 2017). All three trendlines (equity ownership, SIP inflows, and MF AUM) indicate that there is continuing growth of market participation; however, current penetration remains relatively low, with demat accounts covering only ~11% of the total population and indicating there is substantial room for increased (and more risk) growth.

Drivers: Technology, Products & Behavior

Technological advancements, (especially the advent of low-cost smartphones and high-speed internet), have enabled even the smallest of savers to transfer funds into app-based platforms (like Zerodha, Groww, and Paytm Money) within minutes using UPI payments. The emergence of robo-advisors, goal-based planning tools, and social media “finfluencers” has made it easier for novice investors to learn about investing and transact with their money. Financial firms have also introduced innovative products to assist investors: low-cost index funds and ETFs promote passive investing; ELS and ELSS products promote tax-efficient investing; and hybrid or balanced funds provide conservative investors an opportunity to invest using both debt & equity instruments. Furthermore, the financial services industry itself has greatly increased its marketing efforts, leading to many first-time investors participating in the stock market through employer payroll deductions for mutual funds and through mutual funds sahi hai (mutual funds are good) advertising campaigns.

Regulatory changes and fee structures both positively influence the financialization of products. Both commission-free trading for frequent traders have decreased trading costs, creating an environment more favorable for financialization of products. The Securities and Exchange Board of India (SEBI) has pushed down the expense ratio of mutual funds and enhanced disclosures, which makes mutual funds appealing to retail investors. On the flip side, the real rate of return on bank savings accounts has been very low for a long time; deposit rates have consistently been 6–7% while inflation has been greater than 6% for many of those years. This makes bank accounts littered with cash to be a poor long-term investment. In comparison, equities have generated returns of approximately 10–11% over the same period, while 10-year government securities have been providing yields around 7–8% annually prior to 2023, so equities are significantly better than bank deposits after taxes. The development of long-term passive debt funds and portfolio management schemes (PMS) targeting high-income earners indicates a strong desire for financialization; this has also been demonstrated by the significant increase of non-banking financial companies (NBFCs) and microfinance lending, both of which rely heavily on technology-driven underwriting processes, such as mobile credit applications.

Behavioral factors compound these structural drivers. Young investors display FOMO (fear-of-missing-out) from seeing peers double money in markets, and may underestimate long-term risks. After the 2020 Covid crash and rebound, many retail investors (especially in India and the U.S.) embraced SIPs as an emotional hedge, continuing to buy steadily even in down markets. Herding behavior and short-term market “buzz” on social media can override fundamentals for newbies. At the same time, low financial literacy and overconfidence in branded products have led some savers to underestimate risk, as seen later in mis-selling cases.

Risks & Systemic Implications

The financialization process of savings has benefits (broader financial system and increased domestic financing) but also poses some new types of systemic and household risk. One such risk is leverage and overextension. For example, Bank of America pointed out how household borrowing across India grew astronomically over the last few years and greatly exceeded household income. According to FY2024 data, total household debt was approximately 6.2% of GDP – marking the highest level of private sector debt in a decade – and was increased by loans taken out to purchase homes along with personal loans and credit cards; the increase in total household debt surpassed the decrease in gross savings, resulting in net financial savings being approximately 5.2% of FY2024 GDP (down from approximately 7.7% pre-pandemic). In summary, when individuals are deleveraging off of traditional storage means (i.e., holding less cash) and are leveraging off of non-traditional forms of debt (i.e., personal loans), they are potentially increasing the impact of income disruptions should they occur.

Liquidity mismatch and risk illusion issues are another type of concern. Mutual funds, insurance, or housing are not nearly as liquid as cash; the March 2020 market crash showed that (due to the mass redemptions) debt and equity funds were forced to either fund off their funds or suspend operations, resulting in massive losses. Non-Banking Financial Companies (largely > 20% of retail credit) tend to use short-term wholesale funding and in times of crisis (e.g., March 2020) may have an impact on the banks and the large institutional investors providing funding. Concentration risk increased as there were many SIPs and passive funds were index investing (tracking the same stocks): Therefore, if there is a downturn, it would impact all of those portfolios. Globally, due to policy rates between 2022 and 2024 at all-time highs, bond funds and private credit vehicles incurred losses in terms of their value. Consequently, fixed income is not automatically without risk just because of the financialization process.

Case Studies & Regulation

Systematic Investment Plans (SIPs): Conversely, the SIP revolution in India has been largely constructive. It exemplifies bottom-up financialization via disciplined investing. Over FY2017–25, SIP AUM and folio counts exploded (23.5 crore folios by FY2025), bringing many first-time middle-class investors into equity markets. Regulators have generally supported this flow (e.g. by easing KYC, launching direct MF schemes) but also caution on risk concentration. For instance, after twin Global market shocks in 2022 (rate hikes, Russia-Ukraine), the constant SIP inflows helped stabilize Indian markets. The RBI and SEBI now regularly highlight the need for financial literacy so that SIPs are complemented by awareness of risk, and promote equity-behavior rather than panic-selling.

The rapid growth of the NBFC (Non-Banking Financial Company) industry is an additional part of the financialization phenomenon. The purpose of this is to reallocate household savings (through deposits, bonds, insurance) into retail credit and infrastructure projects. The amount of asset value for the NBFC industry has increased from about ₹24 trillion in 2021 to ₹48 trillion as of March 2025. Some of this growth is attributed to the inflow of mutual funds and institutional capital, which means that households are indirectly “saving” via credit products. As a result of these developments, regulators have introduced new regulations such as the Reserve Bank of India’s Scale-Based Regulation framework (2021) that distinguishes between different classes of NBFCs based on risk level and requires greater governance for larger NBFCs. Similarly, the Securities and Exchange Board of India’s new regulations for mutual funds and asset management companies were enacted in order to discourage providing funds for excessive risk-taking by NBFCs. The overall goal of this new regulatory framework is to prevent an NBFC-related credit crunch (as seen with the IL&FS/2018 case or the Yes Bank/2020 case), since today’s households are taking on excess “shadow credit” through the use of different types of products.

Policy Recommendations

Policymakers must balance the nudging of diversification in the financial services sector with solid consumer protection measures, such as enforcing strict suitability standards to avoid the mis-selling of complex or high-risk investment products to unsophisticated investors. Policymakers should also focus on designing interest rates and tax incentives to encourage the accumulation of a core “liquidity reserve” so that households can maintain a financial safety net and not be forced into equity markets. Additionally, creating and promoting financial literacy through measures such as mandatory consumer protection disclosures and risk labels will assist consumers in making informed financial decisions. On a macroprudential level, monitoring average flow rates will help authorities determine if counter-cyclical measures are necessary to address sudden surges into equity or credit markets by using measures such as higher margins, increased capital requirements for non-bank financial institutions (NBFCs), and so forth, to avoid the creation of asset price bubbles. Additionally, some experts recommend the introduction of “rainy-day” tax benefits as an incentive for consumers to hold some of their savings in highly liquid safe instruments in an effort to mitigate the risk that herding will occur when making riskier investments.

Conclusion

The finance aspect of saving is indicative of a significant change in the way that individuals are engaging with money and taking on risk in an economy today. Market related or financial products, as opposed to traditional ones such as fixed rate term deposits or cash based accounts, are becoming more predominant as they are more easily accessible through technology, allows someone to participate easier in the markets due to available access, the concern for inflation, and the desire to generate greater returns. On the other hand, this change in the marketplace presents more opportunity for the average household to participate in the creation of wealth and have greater involvement in their financial lives but also exposes them to increased levels of market volatility and greater levels of complexity and risk. As the use of financial products in everyday life grow, the lines between saving and speculation will continue to disappear. Moving forward, the key is to find a way to balance financial inclusion against awareness of financial products and understanding the risks involved with each type of financial products.

Bibliography

- Reserve Bank of India (RBI). Reports and Publications on Banking and Household Savings.

- International Monetary Fund (IMF). Studies on Financialization and Global Capital Markets.

- World Bank. Open Knowledge Repository: Financial Inclusion and Investment Trends.

- Organisation for Economic Co-operation and Development (OECD). Household Finance and Investment Reports.

- The Economist. Articles on Global Markets, Retail Investing, and modern finance.