Fair value is the estimated price at which an asset or liability would be exchanged between a willing buyer and seller in a neutral transaction under normal market conditions.

Table of Contents

What Is Fair Value?

Fair value is a measure of an asset’s or liability’s worth based on its current market price or an estimated valuation. In simple terms, fair value is not just about the price someone is willing to pay—it’s about the price that is reasonable under current market dynamics and conditions.

It reflects the price at which a willing buyer and seller agree to conduct a transaction in an open and competitive market, considering all relevant factors such as market conditions, risks, and future cash flows.

Uses of Fair Value

Investment Analysis

Financial Reporting

- Assets like investments and financial instruments are often reported at their fair value.

- Fair value helps stakeholders evaluate the real-time financial position of an entity.

Merger & Acquisitions (M&A)

Example of Fair Value in Action

Consider a publicly traded company’s stock with a market price of $50. An analyst uses fair value to determine whether to invest in a stock.

The analyst looks at financial metrics, industry performance, and economic conditions to estimate the stock’s fair value at $45.

Because the market price is higher than the fair value, the analyst believes the stock is overvalued and decides not to invest.

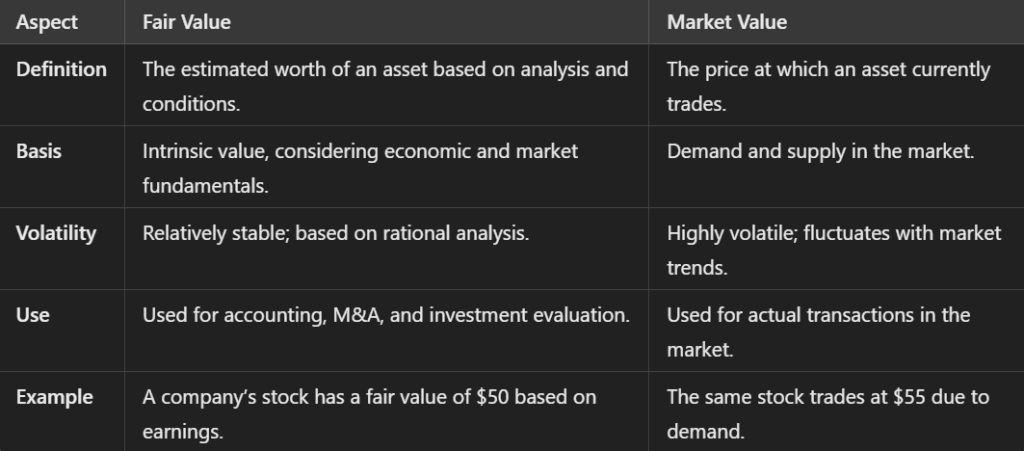

Fair Value vs. Market Value

Fair value is an estimated price derived from financial analysis, considering intrinsic worth, economic factors, and market conditions. It reflects what an asset should be worth in a fair transaction.

Market value is the actual price at which an asset trades in the open market, determined purely by supply and demand dynamics at a given moment.

Benefits of Using Fair Value

Fair value has several advantages. It provides transparency by giving a clear and accurate picture of an asset’s or liability’s worth, which builds trust among stakeholders.

It is also relevant, as it reflects current market conditions, helping investors and managers make better decisions.

Additionally, fair value enhances comparability in financial reporting, allowing easy comparison of different companies and industries.

Challenges

Fair value can be volatile, as it changes with market conditions, which might create fluctuations in financial statements.

For assets that are not actively traded, the valuation can involve subjectivity, relying on assumptions that may not always be accurate.