In 2025, India sees a flurry of IPO, including names like LG Electronics and Lenskart, as well as multiple SME IPO’s. In only 2025, India saw 93 mainboard IPOs up to December 3rd, with reports of a record fundraising total of around ₹1.6 trillion.

As I write this report, Meesho IPO is currently live with an offering of ₹5,421.20 crores.

But there is a growing concern that IPOs are increasingly serving as exit routes and balance-sheet repair tools, rather than engines of fresh productive expansion.

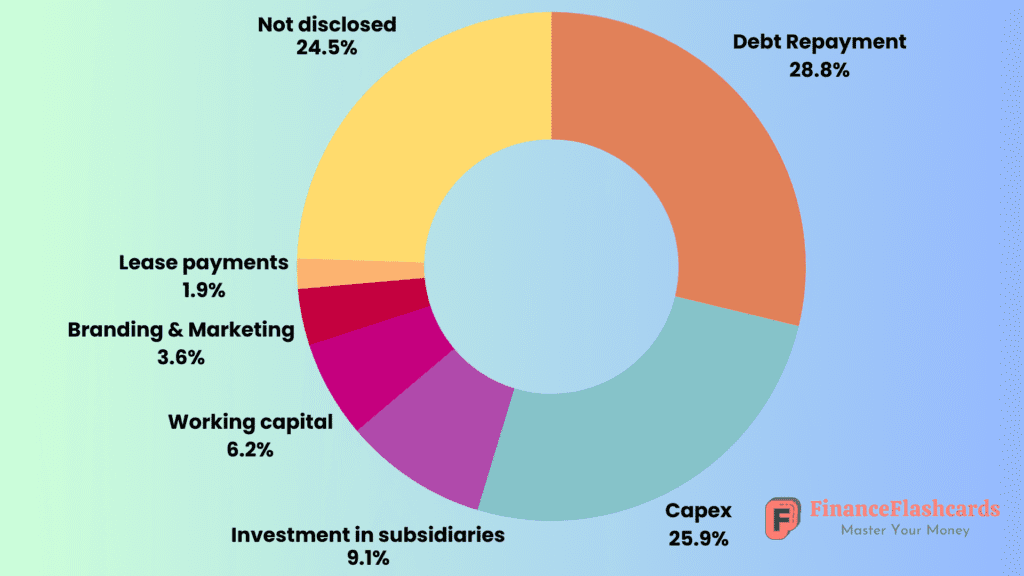

Now according to a report from BoB research, only 25.9% of IPO proceeds are deployed to capex

Key Highlights Of The Report

The study, which analysed a total of 189 IPOs worth ₹1.82 lakh crore in the first seven months of FY26, found that companies planned to raise ₹1.20 lakh crore through fresh equity and ₹62,000 crore via offer-for-sale (OFS).

Of the fresh equity components, only 26% is allocated to capex, while 29% allocated for debt repayments.

Looking at these numbers, the findings echo the comment of chief economic adviser V Anantha Nageswaran, who said that IPOs are increasingly becoming exit routes for early-stage investors rather than a vehicle for long-term capital.

One may argue that offering liquidity to early backers is part of a well-functioning market. True. But when such exits dominate fresh fund-raising cycles, the IPO market becomes less a tool of productive capital creation and more a conveyor belt for investor churn.

Why CapEX Matters

Capital expenditure — the holy grail of growth- is a most important aspect of growth when we talk about young companies. As a young company, you expand yourself and invest in new technology or projects that generate positive cash flows.

Let’s say there are two companies both raise ₹1,000 and A spend all ₹1,000 to invest in new project that earns the company ₹150 every year, which means the project generated a return of 15%, and if the investor who gave the ₹1,000 demands 12%, then the company can the shareholder ₹120 back, keeping the rest, which increases the company values.

On the other hand, let’s take B, who used only ₹250 to invest in a new project, earning the same 15% return, which will be only ₹37.5. You, as an investor, would still want a 12% return, so if the company pays ₹120 out to shareholders, its net cash outflow would be negative, and hence it would lose money.

Now, this shows the classic example of how taking on projects higher than the company’s cost of capital or cost of equity would generate positive cash flows.

None of this is an argument against IPOs.

A thriving primary market is a sign of economic vitality. India needs more companies tapping equity rather than debt, more investors participating in value creation rather than chasing speculative fads.

Deleveraging is healthy. Shareholder exits reflect a maturing capital ecosystem. But a record IPO cycle that produces only a trickle of new investment is not a win. It is a missed opportunity — especially for an economy that needs large, sustained capital expenditure to maintain momentum.

If the majority of IPO profits are not used to expand capacity, the public markets are not fulfilling the developmental role that they are frequently credited with. The lesson is to make greater use of the window rather than shutting it.

Regulators may need to strengthen disclosure requirements for fund deployment. Investors should demand greater transparency about how their money will be used to produce value. And companies must recognise that capital raised in a bull market still carries an obligation — not just to shareholders but to the larger economy.

India’s current IPO boom is fascinating to watch. However, unless more of that capital is channelled into concrete, steel, technology, and invention, the glow will fade rapidly, leaving behind cleaner balance sheets, yes, but not the high-growth future that we continue to expect.

Remember, when the tide turns, only those survive that have built true assets, capacity and positive future cash flows.