Executive Summary

Rehypothecation is the term for reusing collateral that one party (usually a client) has promised to another party for different purposes. In today’s modern financial environment, securities and cash can be exchanged through chains of rehypothecation. For instance, a broker-dealer can take a client’s pledged bond, use it as collateral for a repo transaction, and receive cash as a result. The broker-dealer can then use that cash as collateral for another transaction, and so on. The repeated use of a single asset, such as a bond, creates a multiplying effect; as a result, the asset can back multiple layers of financing and increase leverage in both the financial system and surrounding credit markets. Reusing collateral increases the efficiency of financial markets and increases liquidity within those markets but increases the concentration of risk associated with those assets and can create complications when financial institutions experience crises. Financial crises have demonstrated that when institutions experience extreme rehypothecation of an asset or class of assets, the risks of asset shortfalls and contagion increase when the institution fails or goes bankrupt. Notably, the 2008 financial crisis and numerous other institution failures (e.g., MF Global) have shown how the excessive rehypothecation of an asset class or group of assets results in difficulties recovering lost or mismatched assets for clients who entrust the institutions with their assets.

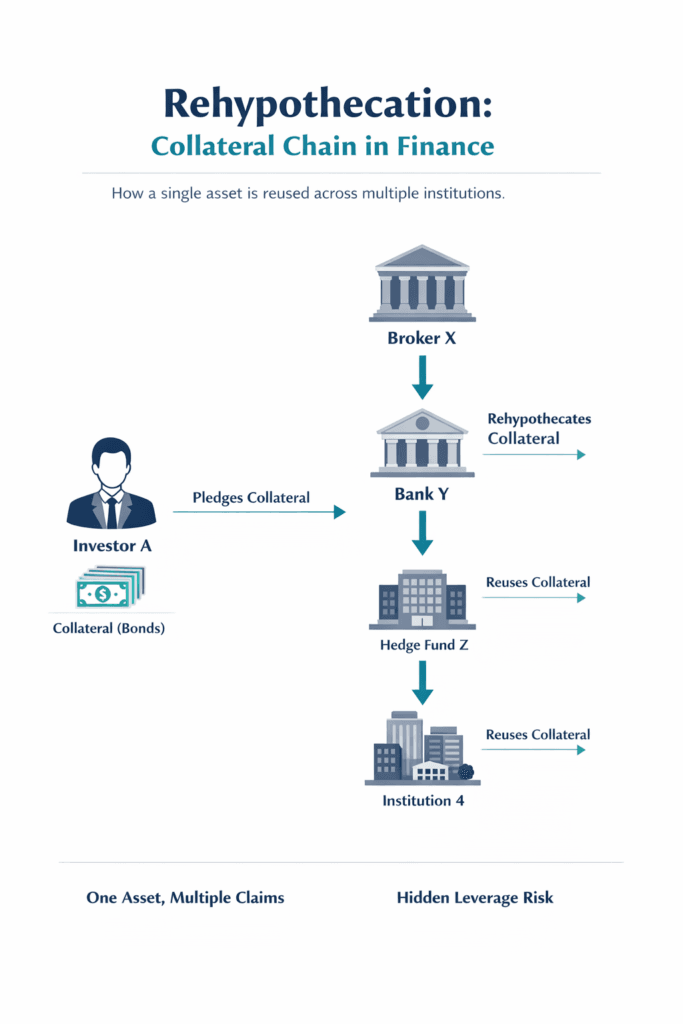

This article discusses how rehypothecation has developed through the repo and prime brokerage markets and gives an illustration of the market structure, including repos, securities lending and derivatives margins. Additionally, it outlines a typical collateral chain with a flowchart. The legal rules vary from jurisdiction to jurisdiction: U.S. regulations prohibit rehypothecating client assets (though this has changed since 2008), while UK/EU jurisdictions have historically allowed this with the client’s express consent (though EU fund custodians cannot now reuse client assets). Finally, we provide quantitative data demonstrating the large volume of rehypothecation prior to the financial crisis. For example, ECB data indicate that large European banks reused approximately 3.8 trillion euros (30% of their total assets) in collateral prior to 2008. Additionally, Fed analysis indicates dealer collateral multipliers for Treasuries range from 6-9 times.

Definitions and Mechanisms of Rehypothecation

Rehypothecation is the reuse of deposited collateral for other transactions by a particular party. The Financial Stability Board (FSB) defines rehypothecation as “any use of customer assets by a financial intermediary,” including broker-dealers, etc. Rehypothecation versus collateral re-use is much broader as it takes into account the reusing of all posted collateral by anybroker-dealer (regardless of whether or not it was customer property). As with most instances of rehypothecation, this will occur when a client (e.g., hedge funds, corporations or individuals) posts collateral (securities or cash) with a broker in connection to the client’s trade; brokers are permitted contractually to repledge this collateral (example being to repo or to secure another loan) subject to the applicable limits.

The utilization of collateral has grown past just client pledges. Once the broker reuses the collateral provided by the client, the receiving party can utilize that same piece of collateral again. Overall, this means one piece of collateral can go through many different hands or exchanges: client, prime broker, dealer bank, money fund, central bank, etc. Each of these steps (most often repo or securities loan transactions) will have a haircut applied to the collateral; however, they will all still be using the same security to collateralise the transaction. When considered in isolation, rehypothecation has enabled one dollar of collateral to generate multiple dollars worth of financing. Using for example, if you have three consecutive repos on $100 worth of collateral and each repo has a 2.5% haircut, you would generate approximately $285 in cash.

The economics of the economy calculates the “Collateral Multiplier” using this equation: Total outflows of collateral (what is taken out of the money supply) / Eligible Collateral for the transaction. The average multiplier of Goods or Services using U.S. Treasuries at most large banks in the US is 6 to 9 times, meaning that if you put $1 into Treasuries, it generates $6 to $9 back into the money supply (based on multi-tiered reuse of that $1). When looking at less liquid or less attractive collateral to the financial system, the multiplier is only about 3 times. With so much uncertainty related to the collateral used for financing due to limited availability of high-quality liquid collateral, the ability to reuse that collateral becomes even more essential in generating available funding. However, collateral reuse also creates challenges for tracing chain links; as collateral is passed along through rehypothecation (collateral being used to support another loan), the original user may not know where their collateral ended up as a result of multiple counterparty or collateral transactions performed before or after where it originally originated, making it difficult for them to recover the collateral in the event of a failure of a major market player.

Physical Assets Rehypothecation has many advantages related to funding costs to brokers and improving liquidity in the market by recycling collateral to where it is needed. Rehypothecation provides dealers ability to meet large cash demands in a smooth manner by providing the ability for them to re-use repos as the main venue of getting cash from the market.

The negative side of rehypothecation involves transparency risk associated with being able to see how many parties have claims on the underlying securities, and therefore if a financial institution has reused collateral, it may have difficulties in quickly unwinding those securities in the event of a counterparty shock. The additional use/reuse of collateral adds to leverage; this creates an interconnection between institutions such that an event at one node of the interconnected network will have a direct impact on another institution. As noted by the Financial Stability Board (FSB), rehypothecation would create an environment where “rehypothecation may serve to create additional leverage and increase the degree of interconnection between firms.” The additive nature of rehypothecation chains will add to the size of shocks; should one institution cause a run on collateral, then all of that institution’s counterparties will rush to reclaim that collateral leading to further runs on collateral by all of their counterparties.

Historical Evolution and Scale

The practice of using the same collateral multiple times has grown in popularity due to the increase in repos, derivatives, and prime brokerages. A substantial increase in the number of prime brokerages began during the 1980s and 1990s with companies such as Goldman and Morgan Stanley driving the growth of the rehypothecation industry, allowing hedge funds to use one pool of collateral to establish numerous lines of credit. Figure from a 2009 law review indicates that U.S. firms had approximately $8 trillion in out on loan securities (via repos and securities lending) as of 2004. This is indicative of the time period of low cost of capital which has been classified as a major aspect of the shadow banking system.

No one was measuring how much collateral was reused (from start to finish) until after the 2008 global financial crisis. Singh(2011) and others have provided an estimate of the “velocity of collateral” (based on data aggregated internationally). However, once the global financial crisis hit, governments around the world became more concerned with understanding the financial markets, including how collateral was used. For example, European Central Bank (2018) found that 11 major international banks had €3.8 trillion of collateral reused in 2007 (~30% of total assets). After the global financial crisis, there was a sharp decrease in collateral reuse (had €1 trillion) due to decreased availability and credit lending. By mid-2010s, collateral reuse had recovered to about €2.5 trillion. This demonstrates procyclicality in that there was a surge in collateral reuse in the credit boom and a sharp drop-off during stress/formal collapse.

The Fed’s examination of big US dealers shows that the large dealers can reuse 85% of all of the collateral they receive from their clients by sending the same collateral back to their customers after being re-used. For instance, the re-use of US Treasury securities (IE Treasury bonds) provides an estimated collateral multiplier of approximately 6-9 times compared to the 3 times for other forms of collateral. This means that on a daily basis, these same Treasury bonds are represented by multiple transactions within the total number of processed transactions. The level of rehypothecation that exists today within global finance (whereby the same US Treasury bonds or other financial assets have been represented in multiple transactions) is producing a virtually anywhere from 2-3 times the total number of items that are in circulation today.

How Rehypothecation Works (Market "Plumbing")

Rehypothecation typically occurs via secured funding markets and trading chains. Key instruments include:

Repo and Reverse Repo: In a repo, Party A sells a security (the collateral) to Party B with an agreement to repurchase later. The seller (Party A) effectively obtains cash, using the security as collateral. If Party A is a broker holding client collateral, it can post that collateral in the repo, a rehypothecation. The receiver (Party B) often is a dealer or bank, which may itself reuse the same collateral in its own repo. The Fed notes that for U.S. Treasuries, the vast majority of encumbered and rehypothecated collateral is transacted via reverse repos and repos.

Securities Lending: Similar to repo, securities lending involves lending securities against cash collateral. Again, the lender can reuse collateral from one transaction in another. Bilateral securities lending agreements in prime brokerage allow hedge funds to borrow securities (with cash pledged), and the hedge fund may re-pledge the cash received, etc.

Prime Brokerage Agreements: Hedge funds open “prime accounts” at large banks. Under the master agreement (CSA, Credit Support Annex), the broker may pledge a client’s collateral (say, stocks or bonds) to other counterparties. The CSA often specifies rehypothecation rights. For example, many U.S. brokerages allow rehypothecation up to a limit; historically British brokers had wider rights.

Derivatives Collateral (CSA): OTC derivatives (swaps, forwards) use a Credit Support Annex. CSA contracts typically define whether collateral posted by one party can be re-used. The 1992 ISDA Master Agreement permits a party to re-hypothecate collateral it has been delivered, if the CSA allows it. In crises, safe-harbor provisions gave non-defaulting ISDA counterparties rights to collateral, which sometimes allowed them to keep collateral delivered to Lehman even though other clients lost out.

Measurement Challenges

Rehypothecation is very complex and involves numerous data-related difficulties such as being able to trace all asset flows from all firms, determine which assets are rehypothecated versus customer-collateral, and net off any two offsetting trades that may be occurring. Dealers have a hard time tagging rehypothecated securities because securities that are held by a dealer within a single asset class are fungible as the Federal Reserve Board of Governors has noted. The regulators use different ways to gauge rehypothecation risks (i.e., through the use of ratios of inbound/outbound collateral from SFT reports). The Financial Stability Board (FSB) and Central Banks are calling for better aggregate metrics on rehypothecation (Financial Stability Board Securities Finance Data Collection Framework).

Another data issue surrounding rehypothecation is rehypothecation can take place off the books (via affiliates or special-purpose vehicles) thereby skirting supervision. MF Global used segregated accounts and inter-company loans to hide the rehypothecation of collateral. Standard audit procedures may not easily detect collateral that was reused. Stress testing models often do not factor in the number of times that collateral has been rehypothecated resulting in an underestimation of the systemic risks.

Conclusion

Rehypothecation, a significant advantage in today’s financial environment, serves as a means for funding and after a liquidity boost to the market; however, rehypothecation creates complex networks of institutions through an interconnected system of shared collateral which can cause issues. The 2008 financial crisis and numerous issues such as MF Global show that if trust breaks down, both clients and taxpayers may be disadvantaged. As we move forward from this crisis, rehypothecation needs to continue benefiting everyone; however, this requires that much greater amounts of transparency and proportionate limits on rehypothecation and much more robust client protections be put into place by regulators and market participants. The only way for regulators and market participants to ensure that the shadow plumbing of the financial system is stronger than ever before is to closely monitor collateral flow and align all parties’ incentives so that firms will be liable for the costs of runs.

Stakeholders need to work collaboratively to establish operating parameters regarding rehypothecation by regulators and to continue increasing data collection related to collateral chains. Market participants need to develop measures of their own re-use of collateral and stress test for sudden freezes. A critical issue will be to understand that not all collateral is created equal, which is what was found by the FSB. The only way for the financial system to continue utilizing collateral as a source of upgrade, as opposed to upgrade to the retail market, is through the creation of better and thoroughly understood collateral chains.

Bibliography

- Bank for International Settlements. (2013). Policy Framework for Addressing Shadow Banking Risks in Securities Lending and Repos (Recommendation 7).

- Commodity Futures Trading Commission. (2014, April 3). Customers of MF Global Inc. to Begin Receiving Final Restitution Payments… (Press Release #6904-14).

- Financial Stability Board. (2017, January). Re-hypothecation and Collateral Re-use: Potential Financial Stability Issues….

- Federal Reserve Board. (2018, Dec 21). Infante, S., Press, C., & Strauss, J. The Ins and Outs of Collateral Re-use. Fed Notes.

- Infante, S., & Vardoulakis, A. (2018). Re-use of Collateral: Leverage, Volatility, and Welfare (ECB Working Paper 2218).

- Office of the Federal Register. (2009). U.C.C. § 9-207(c) (2005).

- Securities and Exchange Commission. (1934). 17 CFR § 240.15c3-3 (Customer Protection Rule).

- Singh, M. (2014). Collateral Scarcity and Rehypothecation (Monetary and Economic Studies, Bank of Japan).

- SIPC. (2012, Feb 6). Status Update from Trustee for MF Global, Concerning the Trustee’s Investigation.

- U.S. House of Representatives. (2012). The Collapse of MF Global – Hearing Before the House Agriculture Committee.