The expected annual return on a bond, assuming it makes all interest payments and repays the original principal, is known as the yield to maturity.

Table of Contents

What Is Yield to Maturity?

YTM or yield-to-maturity is a term used very closely with bonds. It is the internal rate of return (IRR) of an investment in a bond if the investor holds the bond until maturity, with all payments made as scheduled and reinvested at the same rate.

The YTM is based on the belief or understanding that an investor purchases a security at the current market price and holds it until it matures (reaches its full value), with all interest and coupon payments made on time.

Yield to maturity (YTM), also known as book yield or redemption yield. It incorporates the present value of all future coupon payments while accounting for the time value of money.

Calculating The YTM of A Bond

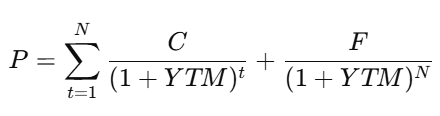

The Yield to Maturity (YTM) formula calculates the annual return expected from a bond if held until maturity. While the formula itself doesn’t have a direct closed-form solution (it requires iteration or numerical methods),

the equation to solve for YTM is

Where:

- P: Current market price of the bond

- C: Annual coupon payment (Coupon Rate×Face Value)

- F: Face value (par value) of the bond

- N: Number of years to maturity

- YTM: Yield to Maturity (to be solved for)

Explanation

- The formula calculates the present value of all future cash flows from the bond, including:

- The coupon payments discounted to the present value.

- The face value of the bond discounted to the present value at maturity.

Since YTM appears as an exponent and cannot be isolated algebraically, it is solved iteratively using:

- Trial-and-error methods

- Financial calculators

- Spreadsheet functions like Excel’s

RATEfunction.

Example in Numbers

For a bond priced at $950, with:

- Face value (F): $1,000

- Coupon rate: 5% (annual coupon payment, C: $50)

- Years to maturity (N): 5

Solving the equation, the Yield to Maturity (YTM) for the bond is approximately 6.19%.

YTM vs. Coupon Rate

Bondholder gets coupon payments for holding bonds, The coupon rate represents the total income a bondholder receives annually based on the bond’s face value, and it stays constant throughout the life of the bond. In contrast, a bond’s Yield to Maturity (YTM) can change over time, as it reflects the bond’s current market conditions and price, while the coupon rate remains unchanged.

Relationship Between Coupon Rate and YTM:

Coupon Rate = YTM

- If the bond is trading at par value (market price = face value), the coupon rate equals the YTM.

- Example: A bond with a face value of $1,000 and a 5% coupon rate pays $50 annually. If its market price is $1,000, its YTM is 5%.

Coupon Rate > YTM

- If the bond is trading at a premium (market price > face value), the coupon rate is higher than the YTM.

- Reason: The investor pays more for the bond but receives the same fixed coupon payments, reducing the effective return.

- Example: A bond with a face value of $1,000 and a 5% coupon rate trades at $1,100. The YTM will be less than 5%.

Coupon Rate < YTM

- If the bond is trading at a discount (market price < face value), the coupon rate is lower than the YTM.

- Reason: The investor pays less for the bond but receives the same fixed coupon payments, increasing the effective return.

- Example: A bond with a face value of $1,000 and a 5% coupon rate trades at $950. The YTM will be higher than 5%.

Variations of Yield to Maturity (YTM)

Yield to Call (YTC) is relevant for callable bonds, where the issuer has the option to redeem the bond before its maturity. This variation assumes the bond will be called early, potentially affecting the bondholder’s total return.

Yield to Worst (YTW) provides the lowest yield an investor can expect, considering the possibility of the bond being called early or maturing prematurely. It’s a conservative measure, useful for callable bonds, as it accounts for the worst-case scenario.

Current Yield offers a simplified view by dividing the bond’s annual coupon payment by its current market price. It doesn’t account for capital gains or losses or reinvestment of coupons, making it a quick, though incomplete, measure of return.

Yield to Put (YTP) applies to putable bonds, where the bondholder has the option to sell the bond back to the issuer before maturity. This variation assumes the bondholder will exercise the put option, providing an expected return based on that action.

Closing Thoughts

A bond’s Yield to Maturity (YTM) is the internal rate of return that makes the present value of all future cash flows, including the face value and coupon payments, equal to the bond’s current market price. YTM assumes that all coupon payments are reinvested at the same rate as the YTM and that the bond will be held until maturity. Bonds can include types such as municipal, treasury, corporate, and foreign bonds.