Welcome to our daily edition of Today’s Wrap here on FinanceFlashcards, where we briefly look at the key headlines from the Financial Markets including the repo rate policy decision at RBI’s MPC meet last Friday, and the surge in Japanese stocks post Takaichi’s record victory.

Alongside, we take a look at the performance of Indian Equity Markets for the day- both broader and sector-wise, as well as the institutional trading activity. Plus we go through the Market Stats and Turnover data as on 9th February,2026 from the exchange, with a look at the Wall Street.

So stick around, and read through..

THE MARKETS – TODAY’S WRAP

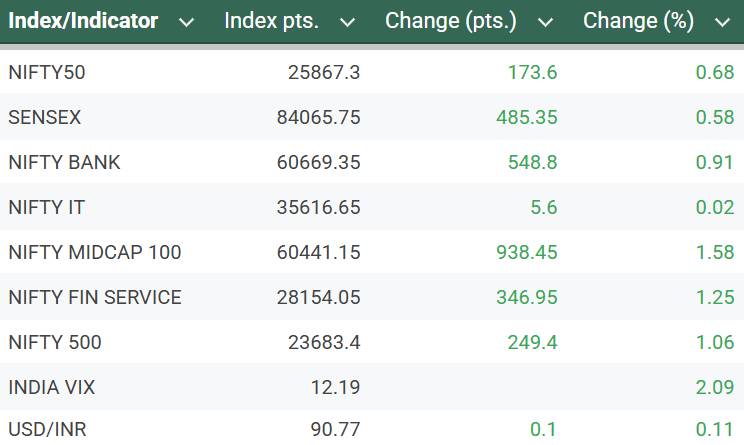

The benchmark equity indices – Sensex and Nifty started the week higher today, amidst positive investor sentiment driven by cues from the recently announced framework of the India-US trade agreement, go along with firm trends in Asian markets. The Bank Nifty index saw a gap-up opening today, outperforming the benchmark Nifty while convincingly surpassing its previous record-high of 60437, ending at ~60670.

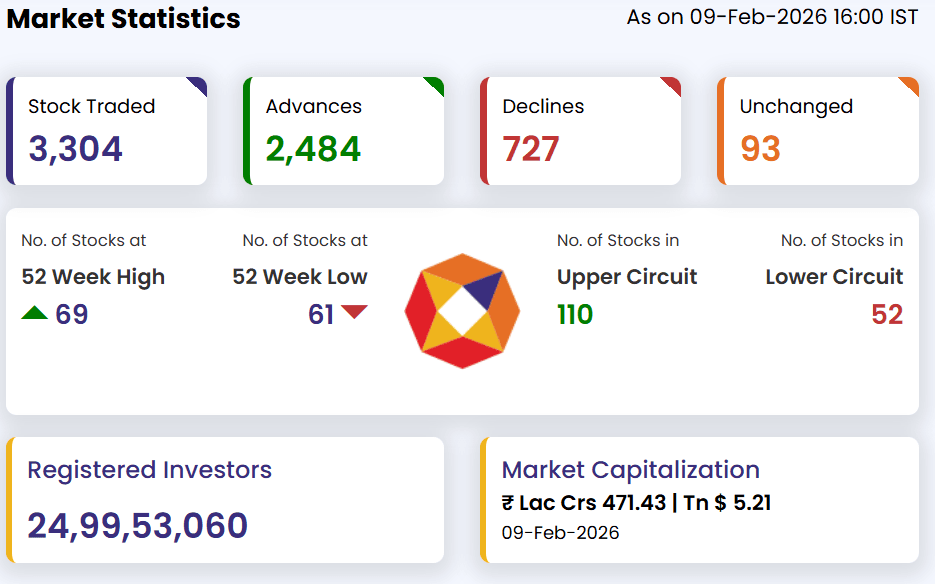

Market breadth was decisively bullish, with the BSE advance-decline ratio closing at a strong 2.45 level, while on the NSE, about 2736 shares advanced, 941 shares declined and 153 shares unchanged. On the currency front, the rupee weakened 11 paise to 90.76 against the dollar, driven mainly by surging precious metal prices fueling importer dollar demand.

Here’s a look at the Market statistics for the day:

Finance Flashcards Newsroom

TOP HEADLINES

- RBI keeps repo rate unchanged at the February MPC meet

On early Friday, the Reserve Bank of India (RBI) left its monetary policy rates unchanged, at 5.25% signalling balance between the economic growth and inflation-check even as geopolitical concerns and upside inflationary risks persist. The RBI at its 59th meet, chaired by the Governor, Sanjay Malhotra, voted unanimously for the policy repo rate with Standing Deposit Facility (SDF) rate also maintained at 5.0%, while the Marginal Standing Facility (MSF) rate and the Bank Rate were left steady at 5.50%. The policy decision was in line with the market expectations, and the reaction was fairly muted on Friday.

The MPC chose to stay neutral in its stance amid global uncertainty, as growth outlook remains robust with GDP growth for 2025-26 estimated at 7.4%. Meanwhile, CPI inflation for 2025-26 is now projected lower at 2.1%, with a temporary uptick expected in Q4 due to base effects. Overall, the central bank signalled a steady approach, choosing to pause and assess incoming data before charting the future course of policy.

- Japanese Stocks surge on Takaichi’s historic snap election victory

Japanese stocks surged to a record high on Monday, as Prime Minister Sanae Takaichi’s Liberal Democratic Party (LDP) basked in a historic election victory. The Japan Innovation Party, the LDP’s coalition partner, won in 36 more constituencies, taking their combined total to 352 seats. The resounding mandate is a gamble that paid off for Takaichi, who now faces the challenge of reviving Japan’s moribund economy and tackling cost-of-living woes.

This led the Nikkei 225 index to rally more than 5% in the early trade on Monday, although the index later gave up some gains to finish 3.9% up, at a record high of 56363.94. Takaichi told reporters on Sunday that she would pursue a “responsible yet aggressive” fiscal policy and would not reshuffle the Cabinet, which was formed less than four months ago. According to BBC, Japan’s economy is under pressure from country’s ageing population, a shrinking workforce and rising social care costs.

- India-Malaysia push local currency trade, sign 11 key sectoral pacts

As Indian Prime Minister Narendra Modi concluded his two-day visit to Kuala Lumpur, India and Malaysia signed 11 agreements to deepen cooperation across key sectors, including semiconductors, defence, healthcare, energy, among others. Both Modi and Malaysian Prime Minister Anwar Ibrahim said the two countries would work to expand bilateral trade beyond last year’s $18.6 billion, step up investments, and strengthen people-to-people ties, including tourism and professional mobility.

According to a report in Fortune India, a major highlight of the visit was the push to increase the use of local currencies for bilateral trade. The two countries also announced a collaboration between NPCI International Limited (NIPL) and PayNet Malaysia to establish bilateral payment linkages. Additionally, both the leaders underlined the importance of the Malaysia-India Comprehensive Economic Cooperation Agreement and the ASEAN-India Trade in Goods Agreement (AITIGA).

EQUITY MARKET DAILY

INDIAN INDICES

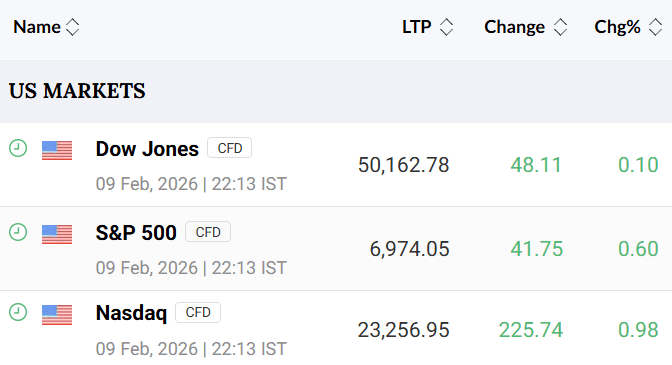

GLOBAL MARKETS

INDIAN MARKETS TODAY

Indices- Benchmark and Broader

The benchmark indices extended gains from the previous session on Monday supported by positive global cues and broad-based buying across sectors. At close, the Sensex was up 485.35 points or 0.58 percent at 84,065.75, and the Nifty was up 173.60 points or 0.68 percent at 25,867.30.

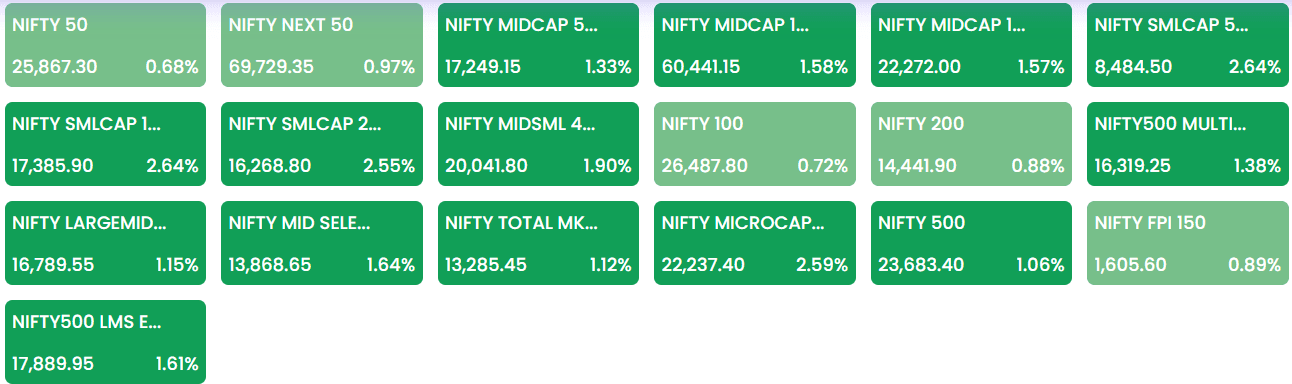

The broader markets significantly outperformed the benchmarks today, with Nifty Midcap 100 climbing 1.58%, while the Nifty Smallcap 100 surged 2.64%.

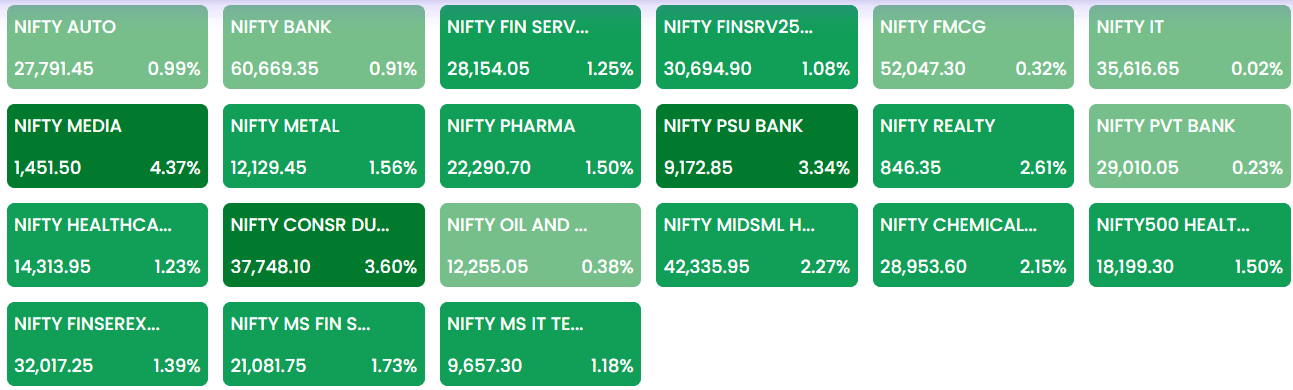

Sectoral and Stock Movement

All the sectoral indices ended in the green with media, consumer durables, realty, PSU Bank, pharma, healthcare, metal up 1-3 percent. The PSU-Bank index witnessed strong buying today, driven by the surge in SBI and Bank of India stocks. While more than 140 stocks touched their 52 week-high including SBI, MRPL, Bank of India, among others.

SBI, Shriram Finance and Adani Enterprises were among top gainers on the Nifty50 while Max Healthcare Institute and ITC were among laggards on the index. The public lender’s shares (SBI’s) shares rose nearly 7% after Q3 results surpassed expectations.

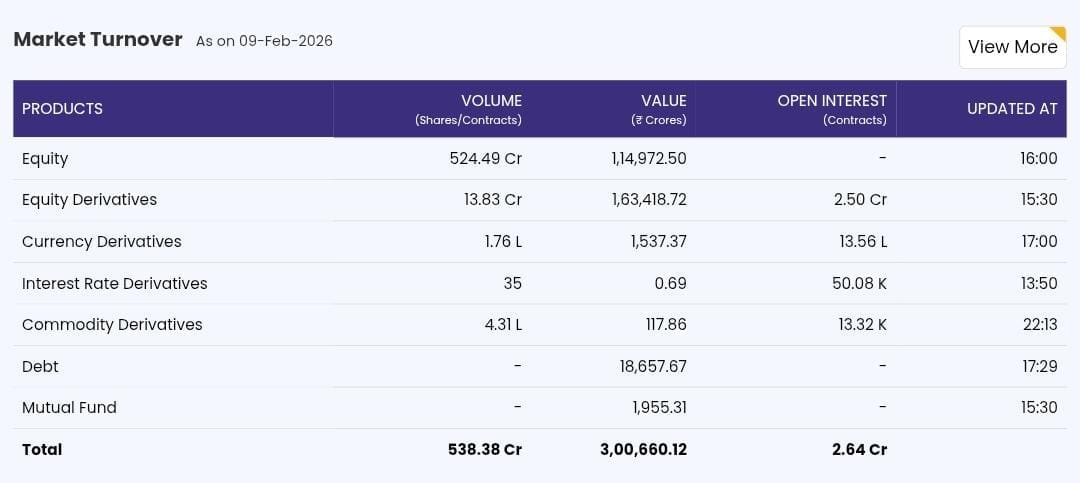

Institutional Trading Activity & Market Turnover

On Monday, the foreign investors (FIIs/FPIs) were net buyers in the Indian Equities, buying stocks worth Rs 2255 crore while the domestic investors (DIIs) net bought around Rs 4 crore worth of equities.

A look at the Market Turnover data is as follows:

That’s all from me in this edition of Today’s Wrap on the Markets. Till next time..

PS: If you like the author’s work and contribution to this platform, and wish to discuss more related to Markets and Macroeconomics in particular, do follow and connect with me, or dm me on:-

LinkedIn @AnudityaGupttaa and X @AnudityaGupttaa