FINANCE FLASHCARDS

Master Your Money

Here is your Weekly Market Wrap of the Indian and Global Equity Markets, along with key headlines that drew attention across the globe. We take a look at the performance of the Indian indices, a recap of the previous week- sector and stock movement, as well as the Institutional trading activity.

So let us get underway..

Market Wrap

Indian benchmark equities extended losses for the fifth straight session on Friday, with Nifty50 falling around 193.55 points (~-0.75%). The Markets continued to be weighed down by relentless selling across sectors, persistent FIIs/FPI outflows along with rising geopolitical concerns including uncertainty surrounding the US Supreme Court’s verdict on the legality of Trump tariffs. While Sensex was down around 604.72 points (-0.72%), the broader indices too underperformed as BSE Midcap fell 0.9% and BSE Smallcap index losing 1.7%.

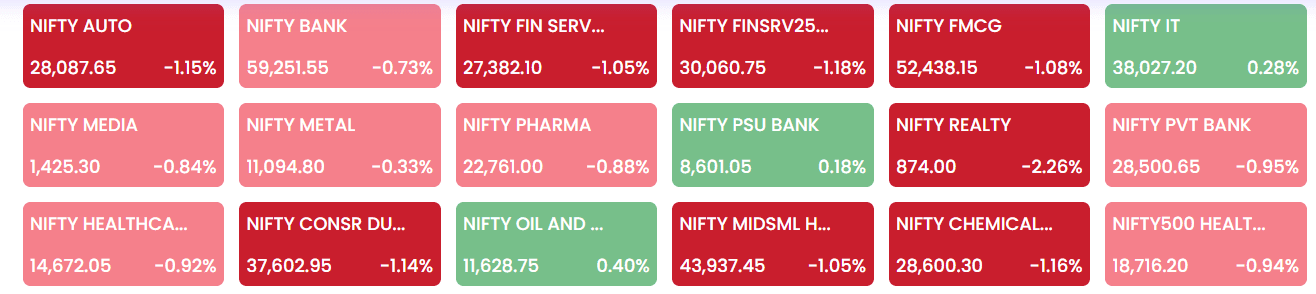

Market breadth was weak: 569 stocks advanced and 2317 declined with almost every sector ending lower, including auto, FMCG, realty losing around 1-2% except IT, Oil & Gas, PSU Bank.

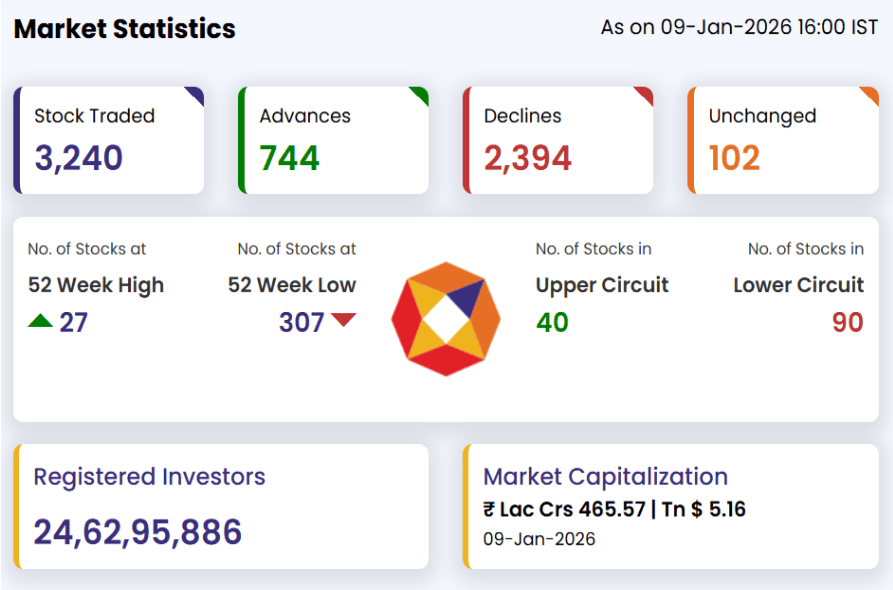

More than 300 stocks hit 52-week low including IRCTC, Siemens Energy, among others while Asian Paints, ONGC were amongst biggest winners on the NIFTY. On the currency front, the Indian rupee closed lower, at ~Rs. 90.26 per USD (down ~0.24%). Overall, the markets today were dominated by weak sentiment, bears’ tightening grip, and rising uncertainty.

TOP FINANCE HEADLINES

- Markets lost 2.5% for the week as Selling continues for the 5th day on D-St.

Indian benchmark indices- NIFTY and Sensex closed at 25683.30 and 83576.24 respectively as losses touched 2.5% for the week. The NIFTY slipped further lower from the 50-EMA indicating rising weakness amidst bouts of selling pressure. And the market sentiment appears decisively negative in the short term.

- India set to be $4T economy in FY26; GDP growth at 7.3%

India’s Real GDP growth above 7% highlighted resilient post-pandemic expansion, well above the 6.5% in FY25. Manufacturing and services drove growth momentum even as agriculture and mining slipped. Although nominal GDP slowed to 8% in FY26, compared to nearly 10% in FY25 limiting revenue buoyancy, growth remained strong in real terms.

EQUITY MARKETS RECAP

Indian Market

As on 9th January, 2025 18:00 IST

Index/Indicator Index Pts. Change(pts.) %Change

NIFTY50 25683.30 -193.55 -0.75

SENSEX 83576.24 -604.72 -0.72

NIFTY BANK 59251.55 -434.95 -0.73

NIFTY IT 38027.20 +106.90 0.28

NIFTY MIDCAP 100 59748.15 -474.40 -0.79

INDIA VIX 10.92 +0.32 3.02

USD/INR 90.26 0.2125 0.24

Global Markets

As on 9th January, 2025 23:00 IST

US Market

Index/Indicator Last Change(pts.) Change(%)

S&P 500 6969.63 +48.17 0.70

NASDAQ 23661.93 +181.91 0.77

Dow Jones 49512.10 +245.99 0.50

European Markets

DAX(Germany) 25324.30 196.84 0.78

FTSE 100(UK) 10131.30 86.61 0.85

CAC40(France) 8352.60 109.13 1.32

Asian Markets

GIFT NIFTY 25820.00 4.00 0.02

Nikkei 225 51939.89 822.63 1.58

Indian Market Brief

1. Indices

BSE Sensex tumbled around 603 points (-0.72%), closing at approximately 83576.24 while broader NIFTY index fell nearly 194 points (-0.75%) closing around 25683.30 on Friday.

The markets extended losses more than 2.5% for the week, as indices fell further on the fifth day of the week owing to rising geopolitical concerns like the tariff fears resurfacing from the US President due to New Delhi buying crude from Russia, along with relentless FIIs selling driving the markets lower leading to negative investor sentiment.

2. Sector and Stock Movement

Most sectors traded below the benchmark owing to negative sentiment while the broader indices also extended losses for the fifth straight session. Additionally, Tariff concerns resurfacing—particularly after the U.S. President Donald Trump stated the possibility of imposing a massive 500% duty on nations buying crude from Russia that brings India into the firing line—triggered risk aversion across global equities, which in turn dampened domestic sentiment.

Among sectors, Auto, FMCG, realty among others lost 1-2% except IT, oil & gas, PSU Bank which traded higher above the benchmark indices. The broader markets remained under pressure too, with midcap and smallcap indices losing around 0.74 to 1.74%, reflecting heightened risk aversion.

3. Institutional Trading Activity

During the session on Friday, FPI/FIIs bought shares worth Rs.11093 crore while selling off Rs.14863 crore worth equities. And DIIs net bought shares worth Rs.18481 crore alongside offloading Rs.12885 crore, as per data on the exchanges.

Finance Flashcards Newsroom

GLOBAL MARKETS

Sentiment fragile as US Supreme Court holds off Trump tariff ruling

The US Supreme court did not issue a ruling on challenges to President Donald Trump’s tariffs on Friday as uncertainty grips markets across the globe. In India, the equities remained under pressure owing to negative sentiment, due to tariff concerns and stalled trade talks with the US. Read more..

Broadcom, other chipmakers drive S&P 500 to record highs

The S&P 500, benchmark US index, rose to record highs lifted by Broadcom rallying 3.8% among other chipmakers, with PHLX semiconductor index (.SOX) jumping 2.7% to record high. Also Alphabet added 1% while Tesla climbed 2.1% lifting the S&P 500 and Nasdaq higher, to 6966.28 and 23671.35 points respectively. The DJIA meanwhile rose 0.48% to 49504.07 points.

For the week, the S&P 500 rose 1.6%, Nasdaq by 1.9% while Dow added 2.3% while investors await clarity on courts ruling on legality of President Donald Trump’s tariffs.

INDIAN MARKETS

Rs 15 lakh cr wiped out as markets log worst week in over 3 months, losing 2.5%

Indian benchmark indices Sensex and Nifty fell around 2.5% this week, the worst in over three months, ending the two week rally. The BSE-listed firms lost market cap over Rs 15 lakh crore during the week, reported Moneycontrol. Fifteen of the major 16 sectors fell during the week, with Oil & Gas stocks leading the losses.

Due to US President Donald Trump threatening to impose 500% tariffs on imported goods targeting countries doing business with Russia, the negative sentiment has led to huge selling in the past two days. India is the second largest buyer of Russian crude after China.

IPO Lookahead: Indo-MIM, Kusumgar, Kissht among 5 IPOs to receive go ahead from SEBI

The capital markets regulator in India, SEBI approved the IPOs plans for five companies with Indo-MIM, Alcobrew Distilleries India, Kusumgar IPOs among them. The SEBI issued observations with respect to processing status on draft papers giving thumbs up to the companies, allowing them to launch their Initial Public Offering within the next one year. Moneycontrol

The Learning of the Day

You would surely know and understand Initial Public Offering (IPO). But did you know,

Most IPOs are a mix of: A Fresh Issue, and An Offer for Sale (OFS)

Let’s take a look at the distinction between these two-

Fresh Issue

Under this, a company issues new shares to the public for the first time and capital raised goes directly to the company. This can be employed for growth, expansion, debt repayment, acquisitions etc.

Example:

If NSE issues 500 million new shares at Rs. 100 each to raise Rs.5000 crore, then it is a fresh issue and money goes to NSE itself.

Offer for Sale

In OFS, existing shareholders (like promoters, early investors, VCs etc.) sell existing shares to the public, implying the proceeds go to existing equity holders and not to the company. In this way, early stage investors book profits or reduce their equity stake.

Example:

If InfoEdge (an early investor in Zomato) sells ₹1,000 crore worth of its existing shares in the IPO, that’s an OFS and here money goes to InfoEdge, not to Zomato.