In early 2026, India’s largest private bank, HDFC Bank, faced a governance meltdown. A probe into the matter found that many of the bank’s senior managers at its Dubai and Bahrain offices have falsely sold the Credit Suisse Additional Tier-1 (AT1) bonds to unsuspecting NRI clients while claiming they were secure deposit accounts. Many investors saw their investments wiped out when in March 2023, the Credit Suisse AT1 bonds were written down by being bailed in (to $0). In March of 2026, the investigation resulted in the surprise resignation of the Chairman of the Bank, Atanu Chakraborty (for ethical reasons; Atanu was also responsible for terminating at least 3 senior Bank executives and disciplining over 12 employees). Many of the conducting investigations eventually got the attention of many regulators. The DFSA from Dubai had already prohibited HDFC’s DIFC Branch from bringing in new clients as of Sept 2025 and the RBI of India issued a statement on Mar 19 stating that HDFC is a professional and well-run organization with no material concerns regarding its governing operations to date. Following the announcement of the findings on HDFC as they relate to the AT1 Bond issue, HDFC’s stock plummeted approximately 8-9 percent.

Background: What Are AT1 Bonds and Why They Matter

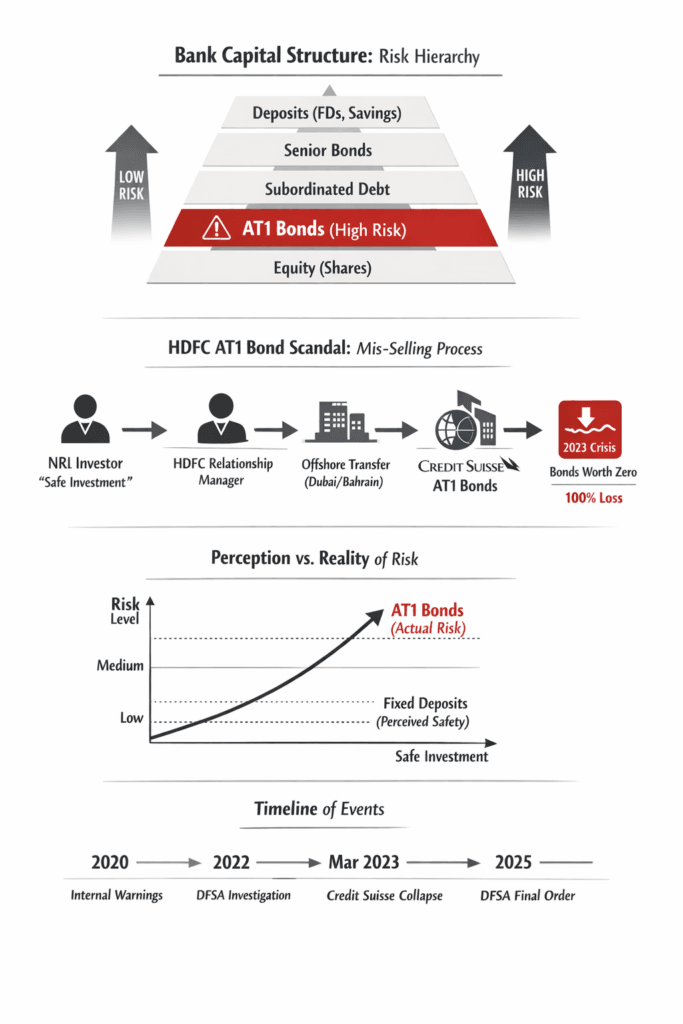

Additional Tier-1 (AT1) bonds are a high-risk form of bank capital instruments introduced under Basel III. These bonds are issued by banks, such as Credit Suisse, and function as a capital buffer, but they have unique features. AT1 bonds are perpetual, with no set maturity date, and therefore offer higher coupons. More importantly, if a bank’s capital falls below a certain level, these bonds can be written down or converted into preferred shares or common stock (equity). As the first in line to absorb losses during a crisis, approximately £17–20 billion of Credit Suisse’s AT1 bonds were bailed in by Swiss regulators during the 2023 UBS takeover, resulting in a total loss of value for investors. As a result, AT1 bonds are significantly riskier than fixed deposits, even though they are sometimes misclassified as such.

In India in the mid-2020s, many investors were unaware of the risks associated with complex instruments like AT1 bonds. Relationship managers from HDFC Bank, operating out of Dubai and Bahrain, reportedly contacted non-resident Indian (NRI) clients and encouraged them to invest in foreign-currency non-resident (FCNR) fixed-income products, often presenting them as offering “fixed interest” and appearing low-risk. However, in some cases, clients were instead sold Additional Tier-1 (AT1) bonds issued by Credit Suisse. Since these bonds could not be directly sold in India, clients had to transfer funds to offshore locations such as Bahrain to complete the transactions. When the bonds were written down to zero during the March 2023 Credit Suisse crisis, many affected NRI investors lost their entire investments.

The Mis‑Selling Scheme and Internal Findings

Through investigatory research reports and internal inquiries—later acknowledged by HDFC Bank and reported in the media, it has been alleged that certain employees abused the trust of customers. Staff members reportedly advised conservative NRI clients with FCNR accounts that the Credit Suisse perpetual bond issue was similar to a fixed deposit offering higher returns. In reality, the Additional Tier-1 (AT1) bonds carried no guarantee of principal and had been classified by regulators as high-risk instruments.

An internal ethics review, along with a concurrent investigation by the Dubai Financial Services Authority (DFSA), found that compliance and audit teams were aware of these irregularities as early as 2020, but the concerns were not escalated externally. A whistleblower letter cited by The Indian Express further alleged that client funds were moved offshore to facilitate the sale of AT1 bonds after concerns about Credit Suisse’s financial health had emerged. It also claimed that while HDFC Bank initially held these bonds on its own balance sheet, they were subsequently transferred to clients who believed they were making safe offshore deposits. When the AT1 bonds were eventually written down, these customers were left fully exposed to the losses.

The actions of senior management have received limited public attention. HDFC Bank has recently made several senior executive changes, including appointments and dismissals involving key personnel: Sampath Kumar, Head of the Branch Banking Division (overseeing global branch operations); Harsh Gupta, Executive Vice President for the Middle East, Africa, and NRI Onshore Business Lines; and Payal Mandhyan, Senior Vice President for the DIFC office (responsible for Dubai and Bahrain operations). These roles were directly linked to the branch networks where the alleged mis-selling took place. In addition, approximately 12–15 other senior and mid-level employees were disciplined for compliance failures, facing actions such as suspensions, loss of pay, and forfeiture of stock options.

In an internal communication, HDFC Bank acknowledged the mis-selling allegations, including concerns related to client onboarding processes at its DIFC office, and stated that an independent review had been conducted.

Regulatory and Governance Response

Regulatory scrutiny surrounding the crisis was significant. Even before the issues became widely public, the Dubai Financial Services Authority (DFSA) had initiated an investigation into HDFC Bank’s DIFC branch in late 2022/early 2023. This investigation culminated in a final order issued in September 2025, which outlined multiple compliance violations dating back to 2020. Due to the seriousness of these breaches, the DFSA barred the DIFC branch from onboarding new clients or conducting new business starting September 26, 2025. The regulator also noted that HDFC’s internal ethics panel had identified the mis-selling as a prolonged and systemic issue, and that the bank had failed to notify authorities despite the practices continuing for over five years.

Following the resignation of HDFC’s chairman, the Reserve Bank of India (RBI) moved quickly to stabilize market sentiment. On March 19, the RBI issued an official statement emphasizing that HDFC remained a systemically important institution with a strong balance sheet and that there were “no material concerns” regarding its overall conduct or governance. Veteran banker Keki Mistry was appointed as interim chairman. Simultaneously, both HDFC and RBI officials clarified through formal communications that the issue stemmed from compliance failures rather than any weakness in liquidity or risk management, aiming to reinforce confidence in the broader financial system.

Nevertheless, the stock market responded quickly to the news with HDFC shares dropping by almost 8.7% right after an announcement regarding the resignation of the company’s chairperson. Further, HDFC shares continued to decline through March. Global institutions such as Macquarie have downgraded their recommendations on HDFC due to concerns about corporate governance. Analysts also indicated that although HDFC’s balance sheet (₹40.9 trillion) and earnings are solid, any remaining doubts regarding the company’s board of directors will likely “weigh” on the stock.

The Mis‑Selling Scheme and Internal Findings

Though limited, the impact of this episode has gone beyond that of the episode itself. Many people believe that the scandal has made it harder to sell Credit Suisse’s write-down cases in Indian courts (because some of the victims are located in India). On top of that, it has also shown that NRI and off-shore channels may be weak points. Therefore, all regulatory authorities (including the RBI and DFSA, along with U.S. Authorities who oversee off-shore branches) should take a closer look at their practices for cross border selling.

The negative effect was caused more by psychological than by economic factors. HDFC Bank, which has historically had a very good image, had been on every global emerging market index as a major company due to its strong performance. Market capitalisation decreases of ₹50,000+ crores (approximately $6,700,000,000) in days was an unmistakable indication that even the strongest banks can experience very large, sharp corrections following disclosures regarding their governance style.

None of the AT1 bondholders were protected by the deposit insurance scheme; therefore, no AT1 bondholders’ loss could turn to be equal to PMC Bank’s loss. Nevertheless, the investors’ trust level has suffered significantly; as a result, the investors who had nothing to do with HDFC Bank sought assurance from regulatory authorities.

Conclusion

India’s banking sector received a rude awakening from the HDFC AT1 scandal. The misuse of a credit instrument exposed the banking industry to significant reputational risk through a hidden chain of credit instrument misuse; this demonstrates that poor monitoring processes will lead to increased deposits bailed out due to reputational risk. Some actionable steps going forward include creating an improved board level risk management awareness; enhancing product-related securities controls; and establishing cross border regulatory coordination. As such, in addition to being vigilant in approving reforms such as more stringent compliance audits, clearly written guidelines regarding AT1 sales to NRIs, regulators must make good on their commitments to restore investor confidence in banks by providing full transparency during future bank “happenings…not in accordance with values”. Ultimately, the best way to maintain confidence in banks is complete transparency: the next time there are bank “happenings…not in accordance with values,” stakeholders expect to see accountability and systemic vigilance quickly.

Bibliography

BFSI Economic Times. (2026, April 3). HDFC Bank penalises 12 execs for role in mis-selling AT1 bonds. ETBFSI.

Bloomberg. (2026, March 18). HDFC Bank Chair Resigns Citing Ethical Differences.

Indian Express. (2026, April 5). AT-1 bond mis-selling case: HDFC Bank acts against 15 executives.

JM Financial Services. (2026, Mar 22). HDFC Bank Fires 3 Senior Executives Over AT1 Bond Mis-Selling Scandal.

Reuters. (2026, March 30). India’s HDFC Bank delayed action in AT-1 bond mis-selling, former chair tells CNBC.

Reuters. (2026, March 19). India’s HDFC Bank says chairman exit may be over rift with management; stock falls.

The Economic Times. (2026, April 3). Dubai regulator probe found HDFC’s DIFC branch kept quiet for 5 years.