Welcome to our today’s edition of the Market Wrap for 11th and 12th February,2026 where we take a look at the key headlines from the Financial Markets across the globe including the sell-off in the IT stocks dragging the markets lower, along with trends from the US Payrolls data, among others.

Alongside, we take a look at the performance of the Indian Equity Market Indices over these two days- both broader and sector-wise, as well as the institutional trading activity. Plus, we also take a brief look at the daily Market stats and Turnover data from the exchange, & at the Wall Street.

So let us get underway with..

THE DAILY MARKET WRAP

The Indian Equity Indices ended flat in a volatile, range-bound session on Wednesday, 11th February. While on 12th February, the benchmarks closed lower amid concerns over impact of artificial intelligence (AI) on IT stocks, as Nifty fell below the 25750 mark and snapped the four-day winning streak. As per analysts, the decline seems more sentiment-driven rather than fundamentals, and despite the better-than-expected January jobs report, the sell-off suggests the reports failed to boost investor sentiment.

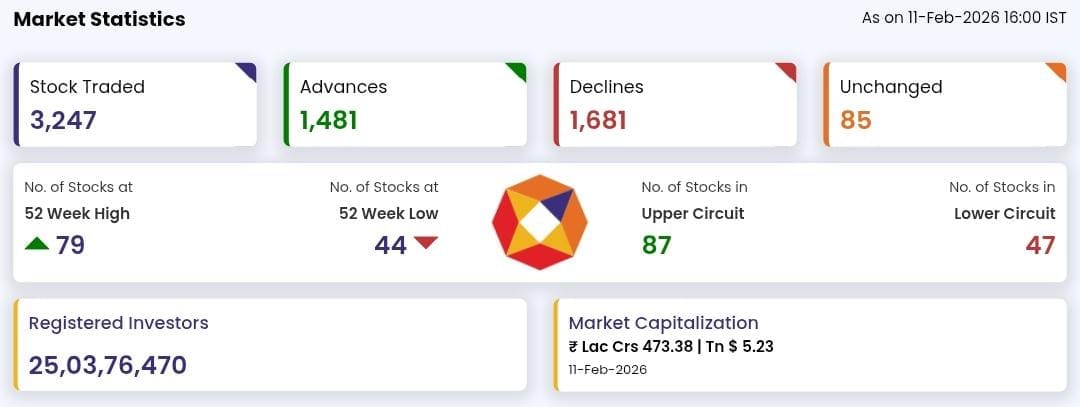

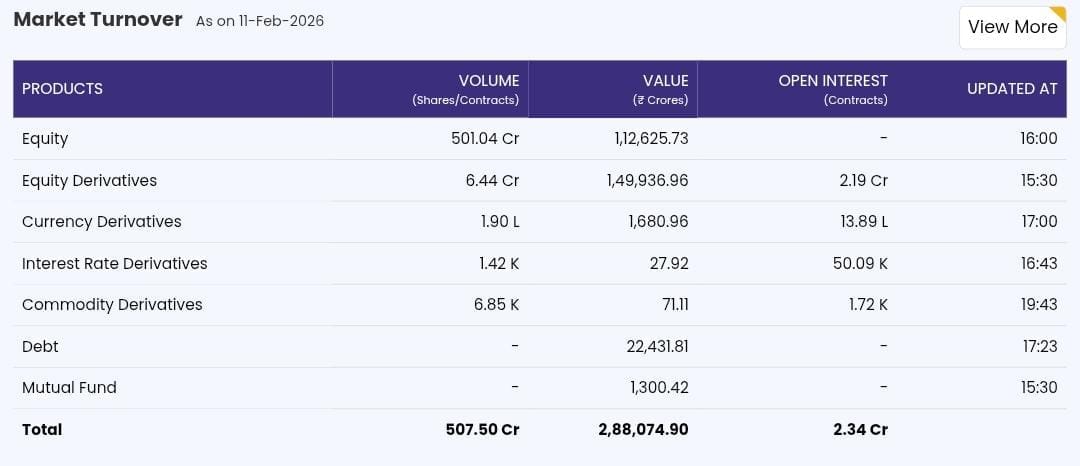

A look at the Market stats for Wednesday..

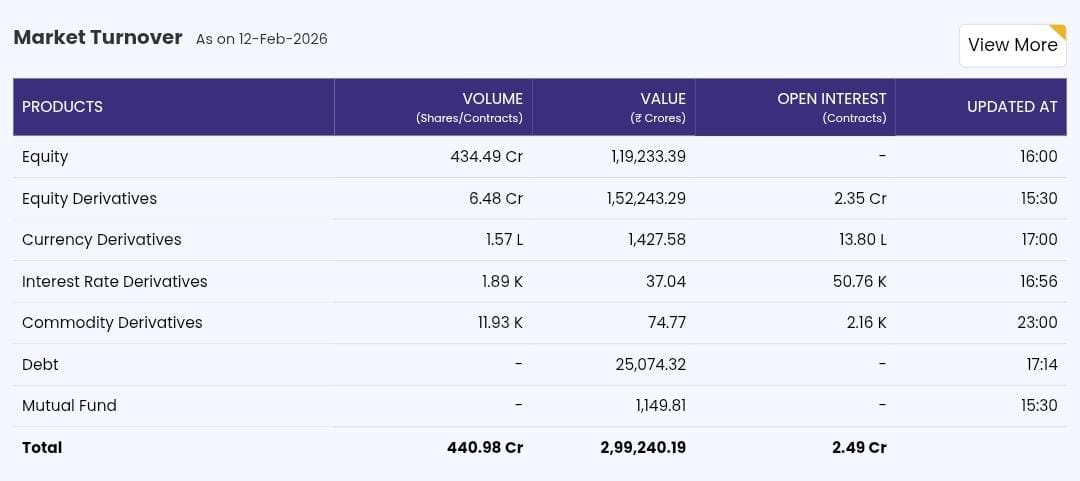

And for Thursday..

Finance Flashcards Newsroom

TOP HEADLINES

Govt. unveils new CPI series with revised weights, January retail inflation at 2.75%

Under the newly launched All India series of Consumer Price Index (CPI) with base year 2024, the retail inflation in India stood at 2.75% in January 2026. According to a report in Fortune India, the revised CPI series expands the consumption basket to better reflect current spending patterns with the number of goods covered has increased from 259 to 308, while services have risen from 40 to 50. The January food inflation rate under new series was 2.13%, with Food and beverages carrying about 37% weight in the index recording 2.11% inflation.

Key enhancements in the new series include the addition of rural house rent and fuels such as CNG and PNG. To improve coverage, digital and administrative data sources have been integrated, covering items such as telephone charges, rail and air fares, postal charges, fuel, and OTT subscriptions.

(FYI: Under the old CPI series with base year 2012, retail inflation had stood at 4.26% in January 2025 and 1.33% in December.)

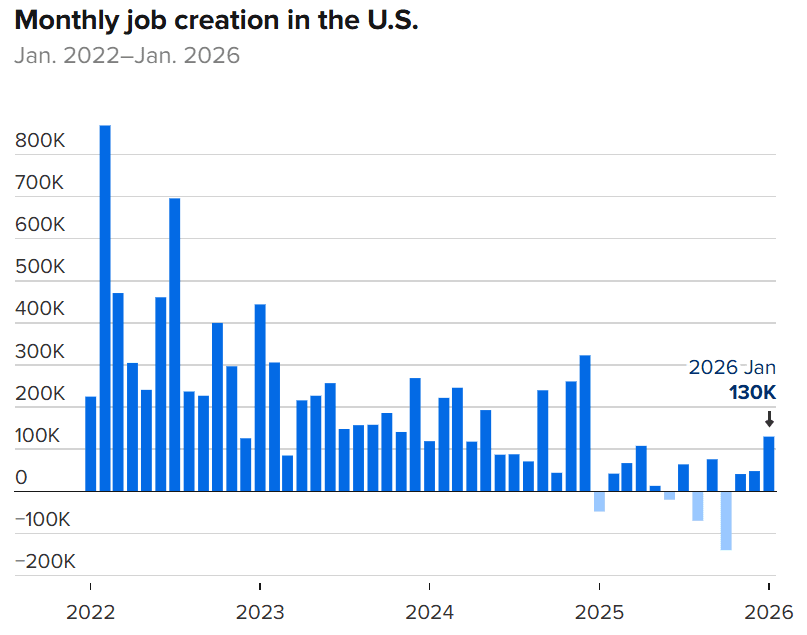

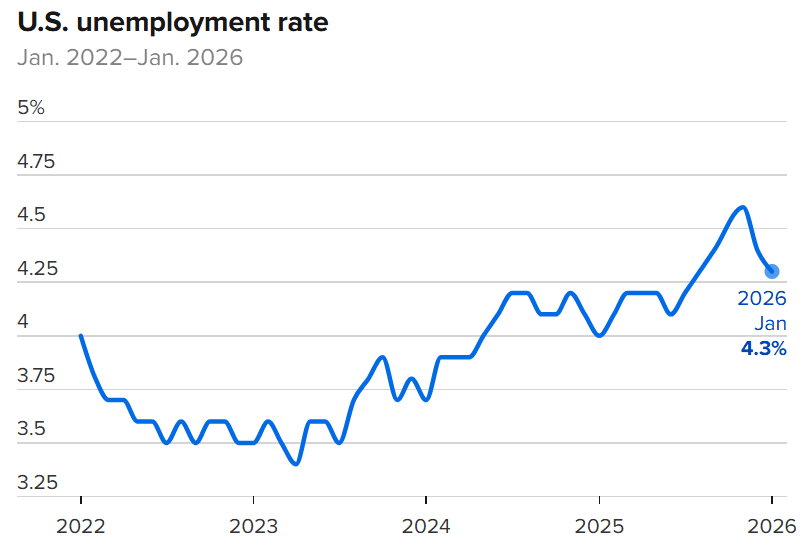

US Payrolls rose by 130000 in January while unemployment falls to 4.3%

The state of US Labor market got a relief after a stronger than expected job growth, as per the data trends from the Payrolls, according to a report in CNBC. According to the seasonally adjusted figured released by the Bureau of Labor Statistics, the non-farm payrolls increased by 130,000 for January, which is well above the Dow Jones consensus estimate for 55,000.

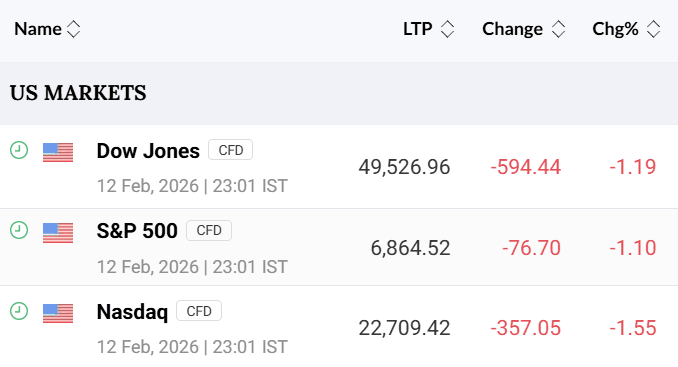

While the unemployment rate edged lower to 4.3%, below the forecast to stay unchanged at 4.4% from the prior month. Following the news, both Markets and treasury bonds registered gains, while the President Donald Trump again called for the central bank to lower interest rates, touting the numbers released as sign of a strong economy.

Tariff revenue soars more than 300% as US Supreme Court decision awaited

In January, the US Government ran a smaller deficit than last year as tariff collections surged, thus providing a reminder of how pivotal a long-awaited Supreme Court decision could be to federal fiscal health. As per CNBC, Customs duties collected through tariffs totaled $30 billion for the month, putting the fiscal year-to-date tally at $124 billion, or 304% more than the same period in 2025. After these duties were first imposed by the President Donald Trump in April 2025 as the so-called Reciprocal tariffs, the White House has been in negotiation mode with its trading patterns.

Even as the Supreme Court is yet to announce a ruling on the legality of tariffs, there’s concern in the White House that a negative ruling could force the U.S. into reimbursing the duties collected so far.

EQUITY MARKET WRAP

INDIAN INDICES

GLOBAL MARKETS

INDIAN MARKET WRAP

Indices – Benchmark and Broader

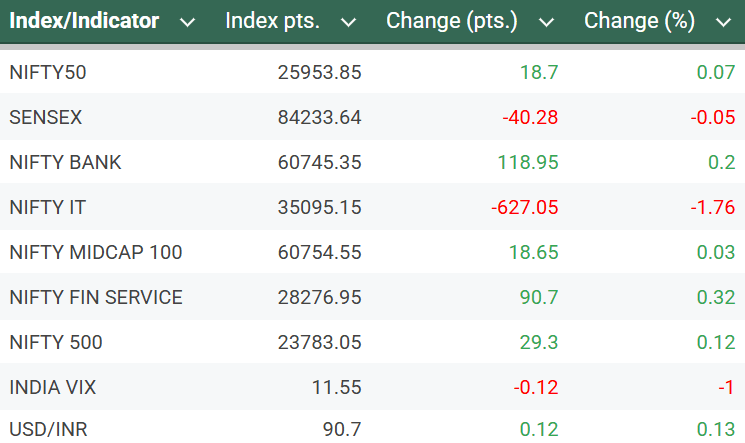

At close on Wednesday, the Sensex was down 40.28 points or 0.05 percent at 84,233.64, and the Nifty was up 18.70 points or 0.07 percent at 25,953.85.

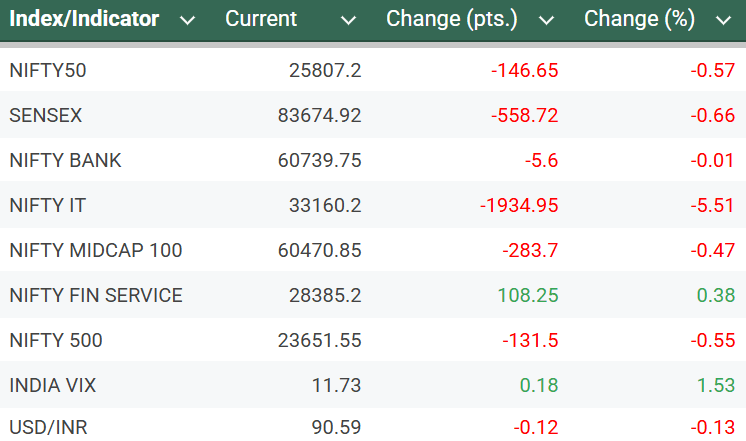

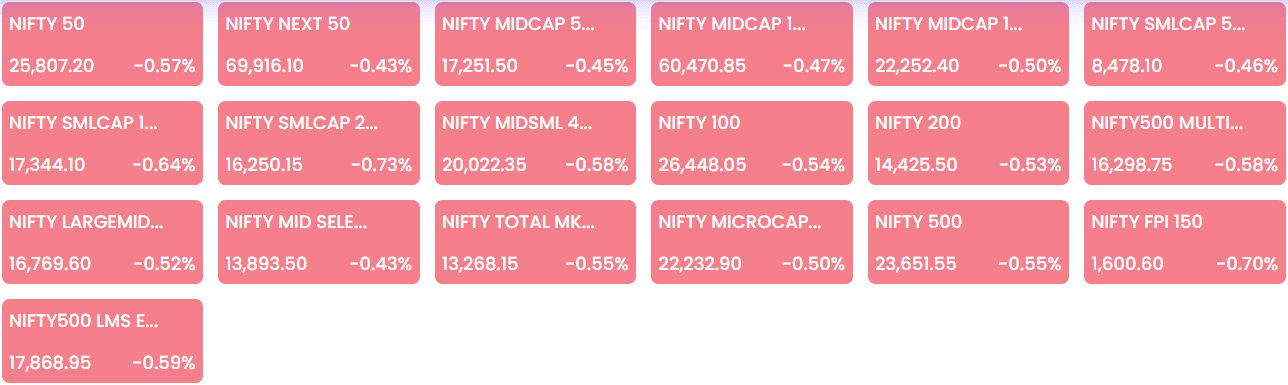

While on Thursday, the Sensex was down 558.72 points or 0.66 percent at 83,674.92, and the Nifty was down 146.65 points or 0.57 percent at 25,807.20 at close. Broader indices performed in line with the benchmarks, with the Nifty Midcap and Nifty Smallcap indices declining 0.5 percent each.

Sector and Stock Movement

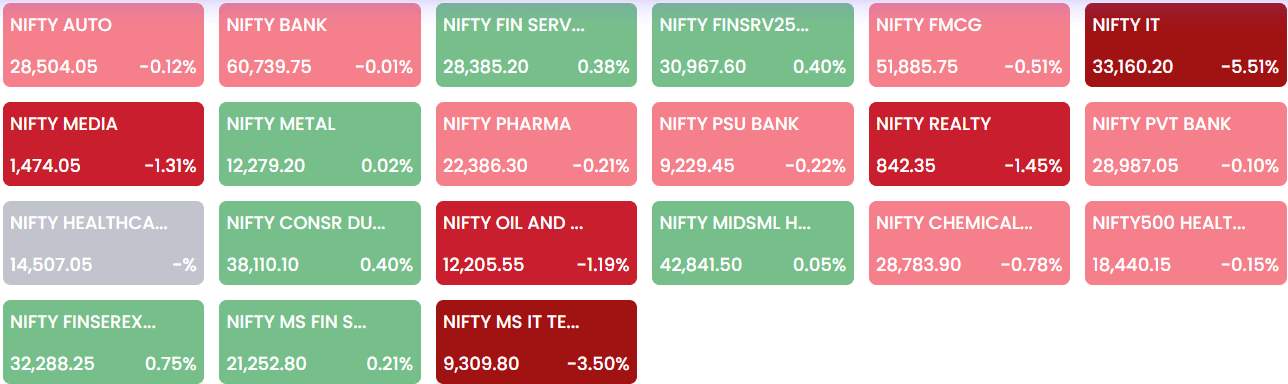

Among sectors, except Consumer Durables (up 0.4%), all other indices ended in the red with IT index sheds 5% and oil & gas, media, realty down 1% each.

Bajaj Finance, Shriram Finance, Eicher Motors, ICICI Bank, Trent were among major gainers on the Nifty, while losers were Infosys, TCS, Tech Mahindra, HCL Technologies and Wipro. More than 130 stocks touched their 52 week-high including Shriram Finance, L&T, ONGC, among others, while about 100 stocks also hit their 52 week-low including TCS, Wipro, Abbott India, among others.

Institutional Trading Activity & Market Turnover

On Wednesday, the foreign investors (FIIs/FPIs) stood net buyers of the Indian equities worth Rs 944 crore while the domestic investors (DIIs) net sold equities worth Rs 125 crore, according to provisional data from the exchange.

And on Thursday, Foreign Institutional Investors (FIIs/FPIs) stood net buyers of Indian equities worth Rs 108 crore while Domestic Institutional Investors (DIIs) pumped Rs 277 crore, according to provisional exchange data.

A look at the Market Turnover data from the exchange..

That’s all from me in this two-day Market Wrap edition. Till next time..

PS: If you like the author’s work and contribution to this platform, and wish to discuss more related to Markets and Macroeconomics in particular, do follow and connect with me, or dm me on:-

LinkedIn @AnudityaGupttaa and X @AnudityaGupttaa