2025 was a year of mediocre performance for the Indian stock market and sharp contrasts: whereas mid- and small-caps, the darlings of the Street until recently, failed, large-caps dominated. Another noteworthy tendency was that domestic mutual funds filled the void left by FPIs’ unpredictability.

For some, 2025 reinforced confidence in equities. For others, it served as a reminder that markets do not reward participation equally. It was a year where size mattered, valuations mattered even more, and selectivity became unavoidable.

A Market That Looked Calm, But Was Anything But

In 2025, the Indian stock market seemed stable at first. Up until early December, the NIFTY 50 produced a yearly return of almost 11%, which was a decent result in a year characterised by geopolitical noise, tight monetary conditions, and worldwide uncertainty. But behind the indices, there was a building crack that was concealed by this surface-level quiet.

Despite being market favourites during the prior surge, mid-cap stocks only produced gains of roughly 5%. Conversely, small-cap stocks fell about 7% during the same time period and into negative territory. One of the most obvious instances of stylistic divergence in recent years was the difference between large, mid, and small capitals.

The timing of this divergence was very noticeable. 2025 marked a clear shift toward quality, balance-sheet strength, and earnings visibility—qualities more frequently associated with large-cap companies—after years of widespread rallies in which smaller businesses frequently outperformed.

Why Large Caps Outperformed in 2025

It was no coincidence that large-cap stocks performed better. It was motivated by both investor psychology and macroeconomic reality.

First, during a period when sales growth for many smaller businesses started to stall, large-cap companies provided relative earnings certainty. Mid and small businesses were disproportionately impacted by tighter financial circumstances, a reduction in spending, and rising input costs. Large businesses, on the other hand, were in a better position to defend margins, pass on costs, and absorb shocks.

Second, liquidity was clearly preferred by investors worldwide. During a portion of 2025, international portfolio investors were net sellers of Indian stocks, but when they did allocate capital, it mostly went to market leaders and index heavyweights. In uncertain markets, mood can change quickly, as seen by liquidity becoming a desirable quality.

FII was a net outflow, and the market was partially funded by DII. Read more here

Lastly, values were quite important. Smaller stocks had little margin of safety due to excesses accumulated during previous rallies. Price adjustments came quickly after expectations subsided.

Valuations Reached Historic Extremes

Valuation stress was one of 2025’s most significant themes. By FY26, India’s market capitalisation-to-GDP ratio had risen to an estimated 135%, the highest level ever. This number demonstrated how costly stocks had grown in relation to the size of the economy and was significantly higher than the trailing five-year and ten-year norms.

Although they alter market behaviour, such high values do not always indicate an impending market collapse. Investors become far less forgiving in high-valuation circumstances. Speculative storylines lose attractiveness, IPOs struggle to maintain listing gains, and companies that miss profit projections risk severe corrections.

In 2025, this was evident. Many recently listed businesses, especially those with aggressive pricing, underperformed after listing. Instead of focusing only on growth, investors increasingly expected profitability, cash flows, and execution.

Domestic Investors Took Control of the Market

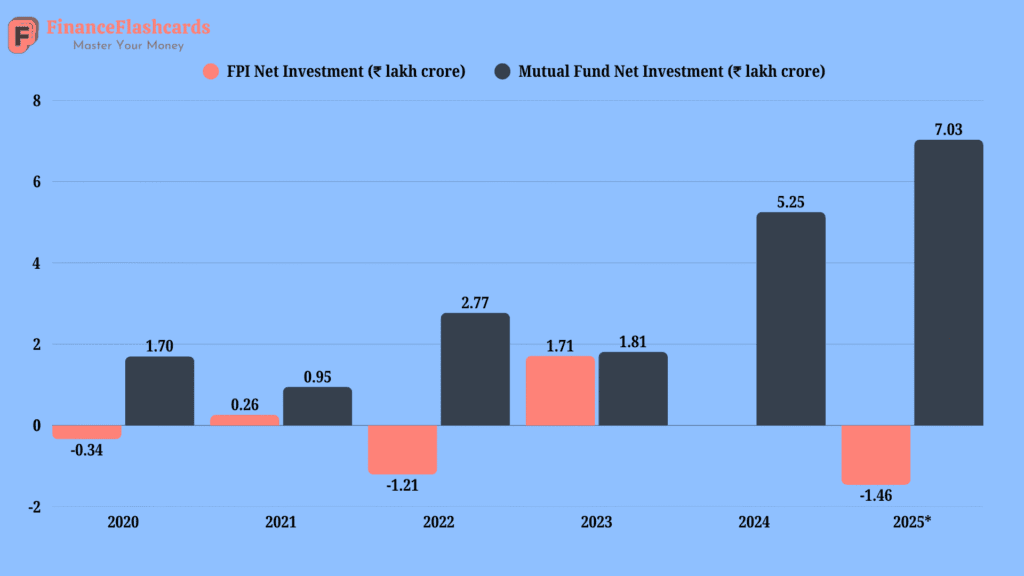

The increasing dominance of domestic capital was another distinctive aspect of 2025. With net stock outflows of almost ₹1.46 lakh crore during the year, foreign portfolio investors continued to exercise caution. Foreign sentiment was impacted by global variables like higher-for-longer interest rates, a strong US dollar, and selective risk-taking in emerging markets.

However, Indian markets did not experience destabilising volatility in spite of this selling pressure. The explanation was straightforward: domestic mutual funds intervened forcefully. In 2025, mutual fund net investments exceeded ₹7 lakh crore, the largest annual inflow to date.

This move is indicative of a structural shift in Indian markets. Domestic investors are becoming a telling force rather than a supporting one due to systematic investment plans (SIPs), growing household financialization, and growing equity awareness. Long-term corrections were frequently caused by persistent FPI selling in previous cycles. In 2025, domestic flows supplied stability by absorbing supply.

It’s crucial to remember that although domestic investors helped the market, they were also picky. The disparity between market categories was reinforced by fund flows that favoured large-cap and high-quality names.

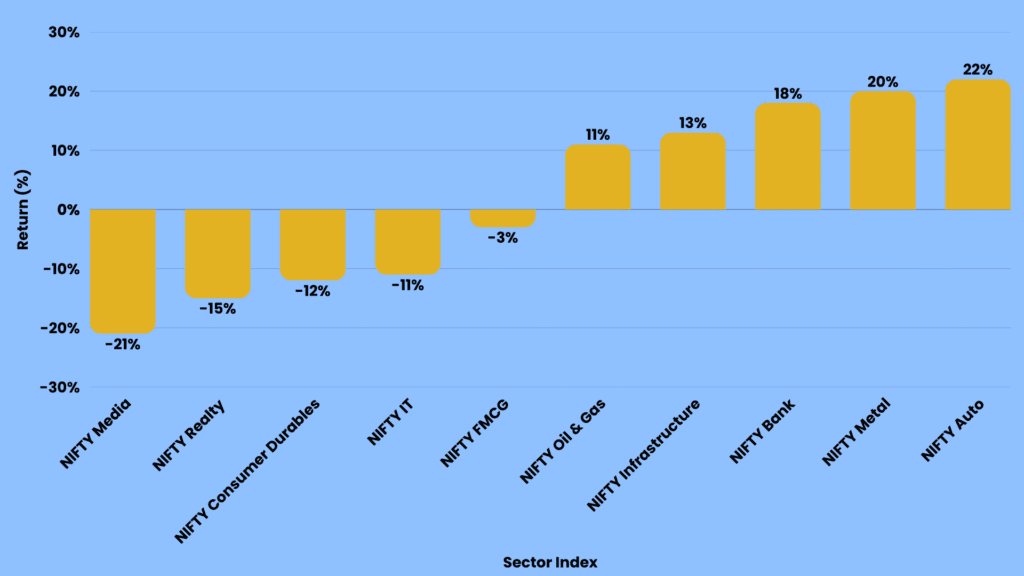

Sectoral Performance Told Its Own Story

The market’s preference for fundamentals over narratives was further supported by sector success in 2025.

Clear winners were the cyclical sectors. Due to volume recovery, premiumization, and increased operating leverage, automobiles produced the best results, with gains of over 20%. Due to both domestic infrastructure needs and global commodities cycles, metal stocks also did well. Stable asset quality, robust credit expansion, and rising return ratios all helped banking equities.

In contrast, several traditionally defensive or growth-oriented sectors underperformed. Consumer durables, media, and real estate all saw double-digit drops, while IT companies suffered as global tech spending slowed. Even FMCG, which is usually regarded as a haven, produced slightly negative returns because of strong base effects and limited volume increases.

This sectoral gap brought to light a significant change: 2025 rewarded economic connection and cash generation rather than predictability alone

What 2025 Means for Investors Going Forward

There are valuable lessons to be learned from the events of 2025. It is impossible to take broad market rises for granted, particularly when values are stretched. Returns may concentrate in a smaller number of stocks and industries, and market leadership may quickly narrow.

The fact that Indian markets are changing may be the most significant lesson. Although they are no longer blind purchasers, domestic investors now have a significant influence on the direction of the market. Capital is becoming more sensitive to fundamentals, more picky, and more conscious of valuation.

2025 was neither a bull market nor a bear market in many respects. It was a market that separated discipline from enthusiasm, strength from speculation, and resilience from excess.